HireQuest was a private staffing company with $190 million in system sales and over 90 locations. In 2019, they merged with a then-public company to enlarge their franchising network and started an M&A spree. Five years later, they have over $600 million in system-wide sales with 430+ branches.

HireQuest franchising model makes acquisitions be much more profitable transactions than they seem to. Instead of rolling up the industry, they are actually rolling it down. The procedure they follow is very peculiar and a fundamental pillar of the thesis on HireQuest.

In this article, I go over:

How HireQuest operates at much higher margins than peers

Intricacies about their M&A system

Analysis of the merger with Command Center

Breakdown of all acquisitions made since going public

How they convert company-owned locations into franchisee-owned

Superior Model

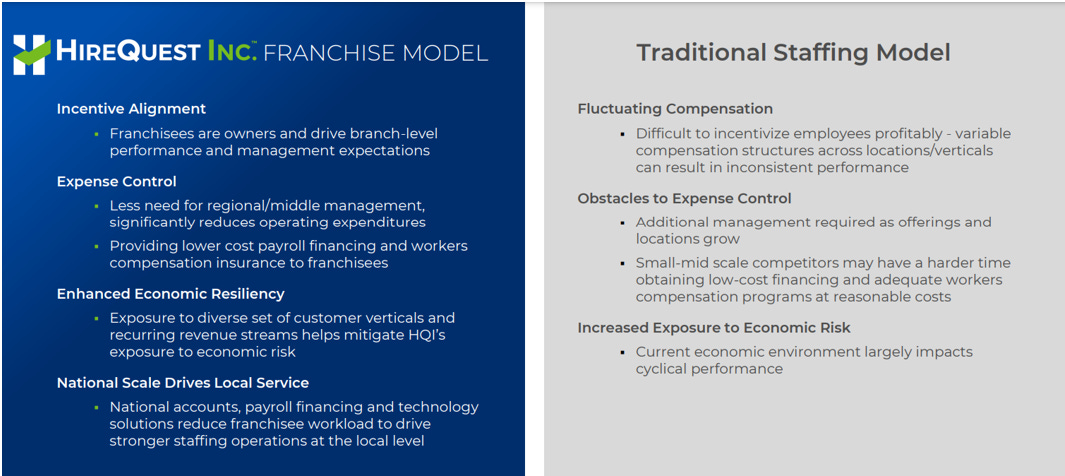

HireQuest finances initial working capital needs to franchisees and leverages their network of offices to access better workers’ compensation insurance, at a cheaper cost per employee. HireQuest does not intend to make a profit from these operations. The company shares the completeness of the efficiency gains from scale with franchisees.

Similarly, management devised a risk management incentive program (RMIP), whereby HireQuest rewards franchisees who maintain their loss ratio below a specified threshold. HireQuest covers up to the first $500,000 in claims, for which a low loss ratio is highly beneficial for them.

Instead of keeping the profit that would come from a lower loss ratio, HireQuest rewards the franchisee by charging them a lower price for insurance coverage. Therefore, not only does the franchisee benefit from a lower cost per policy, but they are also rewarded with an even lower expense. Other programs can provide them with credits on royalties, which HireQuest can comfortably offer due to their scale, helping franchisees improve the economics of their office.

When compared to bigger and more established players, HireQuest differentiate themselves by their pure franchising model. Each office has its respective owner, who’s personally interested in the success of the endeavor. This allows HireQuest to eschew incurring a very common expense present in their counterpart’s business model.

A network of company-owned offices requires hiring branch managers and middle managers to oversee them. When scaled, this gets to be a significant cost, which in turn affects store-level economics. Additionally, it implies increased amounts of working capital investments.

Another advantage HireQuest brings to franchisees is the capacity to leverage scale in order to get national accounts. Corporations that operate in multiple states or require national-wide staffing services tend to forge relationships with large-scale staffing businesses, who can supply them with on-demand labor as it fits their needs.

HireQuest’s franchising network puts them in advantage with respect to small players. Historically, these larger clients have tended to show pricing power when transacting with local staffing companies. By being part of HireQuest network, franchisees end up getting more access to big clients and better deals.

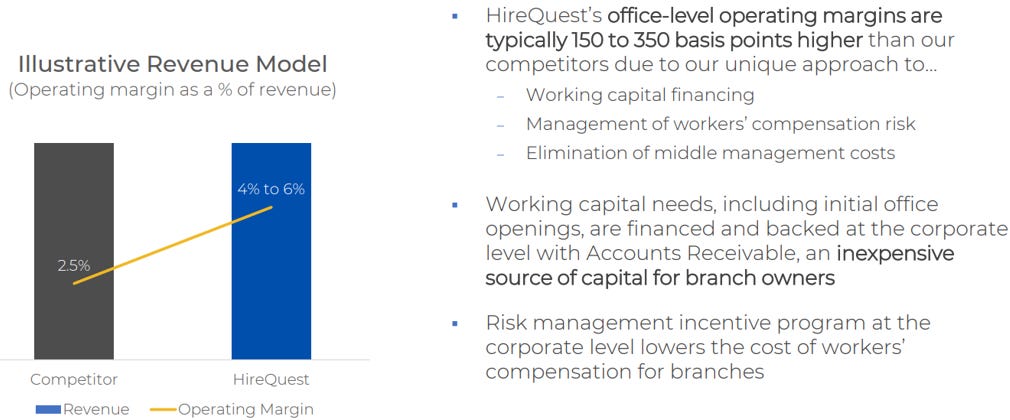

Better office-level economics translate into HireQuest enjoying higher margins on total system-wide sales. I must hereby observe that Robert Half, a public staffing company with company-owned offices, actually has a 5.4% LTM operating margin, but has operated much above this level for the past years. In contrast, ManPower’s operating margin has been between 2-4% in the past 5 years.

“And that's why when you look at, for example, Command Center as an example, is about half the size of HireQuest. It had about six regional managers. We had one. And so, to give you a sense of that, that means that if effectively Command Center was paying something close to six tenths of a percent just for regional managers, we were paying something like one tenth of a percent. That's a big difference when it comes to ultimately to your bottom line, and that's why we're able to offer the same efficiencies to our franchisees (…) And yet without the need to have this big regional, you know, sort of all these regional managers. And the point is, is everybody makes more money is really what it comes down to”

The Merger

HireQuest’s management team has done numerous acquisitions since the company’s inception in the 90s. Ever since going public, they have doubled down on inorganic growth. However, their M&A transactions are quite uncommon. Furthermore, individual offices experience massive economic changes due to HireQuest’s model. To shed some light on this vastly relevant aspect of the business, I’ll dive into the merger with Command Center.

When HireQuest acquires a staffing business with company-owned locations, these need to be converted into franchises. In consequence, the first thing Richard looks for when engaging in M&A is whether he’ll be able to successfully sell the offices. Ideally, they’d be sold to offices’ current managers or people familiarized with the operations of that particular branch. Otherwise, management ask other franchisees if they’d be willing to buy the location and add it to their portfolio. Deals of both kinds may carry unique arrangements. Occasionally, this cannot be done and HireQuest marks the location as a discontinued operation and held for sale.

HireQuest merged with Command Center in July of 2019, keeping the first of both names. Command Center issued 9.8 million shares that were transferred to HireQuest security holders. This meant HireQuest ownership of the combined entity was 68%.

After the merger, it was contemplated that HireQuest would commence a self-tender offer to purchase up to 1.5 million shares at $6 per share. The tender was fully subscribed and the company ended with around 13 million shares of common stock. After the tender, HireQuest security holders owned approximately 76% of the entity, with Richard owning over 43%.

At the time of the merger, HireQuest had over 90 locations, while Command Center reported 67. Even though Command had two thirds of HireQuest’s footprint, HireQuest had more than double their system-wide sales. On a per unit basis, individual offices generated more revenue within HireQuest network. Considering the fact that both served somewhat similar markets, it’s fair to speculate that the incentive structure HireQuest has may have tilted operators into this result.

On average, each of HireQuest offices had revenue of $1.9M, whereas Command Center branches, $1.45M. Richard pointed out during an interview that the main reason behind this large discrepancy is turnover. Turnover severely affects staffing companies; for, as a natural consequence of why employees look for these jobs in the first place, they are very difficult to retain. The difference lies in how much effort a branch manager puts into retaining employees and in finding replacements rapidly, as well as capitalizing on potentially new relationships with clients.

I have hitherto laid down some of the reasons why the franchising model is superior to its counterpart. Per unit sales financially captures this point, but the efficiency at which the whole system works does so as well. Before the merger, during the fiscal year of 2018, Command Center had net income of $974,000, whereas HireQuest reportedly generated $7.1M in profit. HireQuest thereby produced $0.0375 in net income per dollar of office sales, whereas Command Center had $0.01 per dollar of branch sales.

I must observe that, in 2017, HireQuest had net income of $2.88M on $170M in system-wide sales. The huge factor that contributed to 2018’s massive increase in profit was a reduction in one SG&A item by several million dollars, namely management fees. In 2017, $3.4M were paid in management fees, compared to $249 thousand in 2018.

HireQuest’s business model superiority was in fact so notorious that Command Center’s board of directors advocated for the merger occurring partly because of this. Some years before the merger, a group of people had been corporately set to evaluate how could Command Center turn the situation around. Almost two decades of operations had passed and no executive could figure the system out, generating very poor results for shareholders as a result.

As part of the merger agreement, Richard asked Command’s CEO to help him during the transition phase. This is one of the operational risks that exists when making these types of deals. Turning dozens of branches from company-owned to franchisee-owned is not simple and can very well impact HireQuest’s operations. With this in mind, Hermanns tries to secure the conversion beforehand.

Branches Conversion

The merger effectuated in July of 2019. Already by October of that year, the executive team had converted all company-owned locations into franchisee-owned. For the sale of these branches, HireQuest received an aggregated payment of $16.2 million. Most was paid with 4-5yr promissory notes, while some had unique arrangements. More importantly, these branches thereafter operated under HireQuest’s umbrella, benefiting from workers’ comp, software, and working capital solutions. In exchange, the pay a royalty fee. The agreed-upon fee was also generally standard, though there were a few unique clauses.

Branches were converted on three separate general agreements, which occurred on differing dates. The first and almost immediate one was in July, when approximately 31 offices were sold for a total of $4.7 million, paid with 4yr promissory notes at a 6% rate.

In this transaction, I must observe, an entity called World Buyers purchased franchise assets for around $2.2 million. World Buyers represent what management calls “World Franchisees.” This is a small group of people that own an interest in some of HireQuest’s franchises; including Hermanns’ immediate family members and Edward Jackson, who has been involved with HireQuest for over two decades and owns over 15% of the company. As of 2023, Worlds Franchisees were 34 and they operated 70 franchises.

“Based on their respective ownership interests in the Worlds Buyers, this corresponds to a value of approximately $1.132 million for Mr. Hermanns’ children and approximately $0.461 million for Mr. Jackson”

The second transaction occurred in September, when approximately 27 locations were sold. HireQuest received an aggregated payment of $9.7 million, paid with 5yr promissory notes at a 6% annual rate.

Shortly thereafter, the last deal was made, where an approximate of 4 offices were sold to franchisees. HireQuest received an aggregated payment of $1.8 million in the form of 4yr promissory notes at a 10% annual rate.

“Our team worked expeditiously to gain state regulatory approvals and convert the acquired Command Center branches to our franchise business model within 10 weeks following our merger,” Rick Hermanns in October of 2019

The franchising model shows greater aptitude for an acquisition-driven business because managers tend to stay running their branches. When a staffing company with company-owned offices acquires another staffing business with company-owned locations, it’s common for people in charge of the latter’s branches to leave. This is massively damaging, for it’s likely that those people were the ones who kept the customer list together. It becomes very deceiving to acquire under these conditions. What seems like a $10M staffing business may turn into a $3M business after these people leave.

When HireQuest acquired Command Center, most branches kept being run by the same people. This operating framework largely removes the biggest risk when acquiring staffing companies. A transaction involving two staffing businesses with company-owned offices may require an additional 12-24 months just to get back to their prior level of business. Richard mentions that, although it was (in 2021) very hard to tell with Command Center because of the pandemic, sales at the different branches held up very well.

What I would argue occurred with Command Center is that shareholders ended up having more profit per branch. Removing middle managers, increasing efficiency with software and providing cheaper capital to offices translated into more cash flow per unit.

Although this was a merger, for which the following does not precisely applies, the income received from the sale of branches causes the price paid for an acquisition to not be illustrative of the true economic cost for shareholders. This is something Hermanns has done repeatedly over the past 5 years. He seemingly pays a certain price for locations but, after converting them, the price paid ends up being meaningfully lower.

After the merger consummated and the tender finalized, the combined entity had an approximate market capitalization of $80 million. HireQuest security holders owned 76% of the total, while Command Center shareholders owned the remainder 24%. This becomes very illustrative of the true economics behind each of both business models. With 98 locations, each branch in HireQuest network was assigned a market value of $620,000. In counterpart, each location in Command Center’s network was assigned a market value of $286,500.

Link and Snelling

In 2021, after Command Center was fully integrated and the pandemic effects diminished, Richard began re-acquiring staffing companies. During the first quarter of 2021, two significant purchases were made, adding several dozen locations to the network.

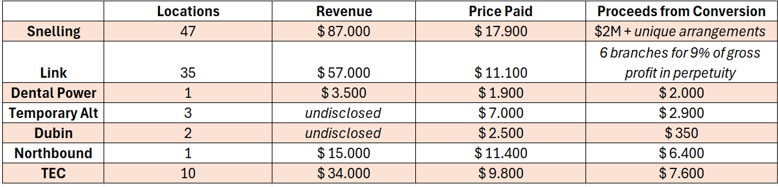

The first company acquired was Snelling, and the trademark remained unchanged. Snelling had around $87 million in system-wide sales and 47 locations. HireQuest paid $17.9 million for Snelling-related assets. Snelling run a franchising business model, but it counted with 10 company-owned locations. To de-risk the transaction, Hermanns decided to sell these 10 branches to third parties. In exchange, HireQuest received:

$1M in promissory notes at 6%

$1M in cash

1.5% of NTM revenue at the Ontario locations

2.5% of NTM revenue at the Tracy and Lathrop locations

2% of revenue at the Princeton for next 36 months

The second acquisition that HireQuest did in March of 2021 was Link Staffing, a multi-decade family-owned business. Link was fully run on a franchising business model. HireQuest acquired the franchising agreements of 35 locations as well as certain other assets for $11.1 million.

To further de-risk the whole operation, Hermanns signed the California based franchise agreement. HireQuest agreed to sell 6 LINK and 1 of Snelling’s branches to a third party. In addition, the remaining 3 Snelling locations in California were sold to the same third party. The buyer became the franchisor of all locations, but agreed to pay HireQuest a royalty fee equivalent to 9% of their gross profit in perpetuity.

The pandemic severely impacted companies who require physical attendance to their work sites. In consequence, the staffing industry highly contracted during 2020, which had leftover effects thereafter. In 2020, Manpower, whose earnings had been around 500M for the previous 4 years, had earnings of 23M on 18bn in revenue, down from 20bn in 2019, and some quarters with sales declining 30%. On the other hand, Robert Half, a very well run staffing business, had revenues contracting over 20% and earnings falling by over 50% YoY during the second quarter.

While it also affected HireQuest operations, the company kept running at over 20-30% operating margins, generating significant amounts of cash. In addition to this, HireQuest is run on the peculiarity that, when franchisees don’t expect much business in the coming months, they refrain from hiring. This stops HireQuest’s cash outflows and the collection of receivables causes a rapid inflow of cash.

Hermanns runs HireQuest in a way that minimizes the operational risk. He tends to fund acquisitions and growth initiatives with generated cash and almost never incurs large levels of debt. Therefore, although the company is affected by calamities such as the pandemic, HireQuest is usually one of the least affected companies. This puts them in a position of strength that Richard takes advantage of to acquire other staffing businesses that become distressed. Importantly, given the fact that almost all staffing companies are struggling at times of distress, there rarely is much competition for the deals Richard goes after.

This is what happened with Snelling. Snelling was struggling financially and was in need of capital. HireQuest offered Snelling’s team to buy the company and advance $2.1 million so that they could pay accrued payroll liabilities. The price paid for Snelling was $17.8 million, meaningfully below the asset value of the business. Consequently, HireQuest recorded $5.6 million as bargain purchase.

“The bargain purchase is attributable to the financial position of the seller and because there were few suitable potential buyers.”

Other Acquisitions and Branch Conversions

HireQuest acquired Dental Power’s staffing division in December of 2021 for $1.9 million. Richard’s intention was to run it as a company-owned location for some time, using it as a platform to launch HireQuest health, and sell the assets for it to become franchisee-owned.

During the fourth quarter of 2022, HireQuest began holding the assets for sale and effectively sold them in March of 2023. A franchisee within MRI network acquired Dental Power from HireQuest at a price of $2 million, payable over 5 years. HireQuest recognized a gain of $340 thousand on the transaction and Dental Power’s branch is now franchisee-owned.

In January of 2022, HireQuest acquired Temporary Alternatives, the staffing division of a family-owned company based on Texas and New Mexico, for $7 million. It’s worth noting that this included $2.6M in accounts receivable. Temporary Alternatives had three company-owned locations which HireQuest sold for $2.9 million immediately after the acquisition. The buyers entered into franchise agreements with the company.

The following month, HireQuest acquired The Dubin Group and Dubin Workforce Solutions (collectively “Dubin”) for $2.5 million. HireQuest split the business into two separate ones, each counting with their own location. Immediately after the acquisition, HireQuest sold the Workforce Solutions segment, specialized in temporary labor, to a new franchisee for $350,000. Management has not yet found a buyer for the other location. In the meantime, HireQuest entered into an agreement with Dubin’s seller for him to continue managing the location as company-owned.

“We are delighted that Kenny Dubin, the founder of these companies, has agreed to stay on to help further develop these offerings."

HireQuest acquired Northbound Executive Search in February of 2022 for approximately $11.4 million. It’s worth noting that this included $3.4M in accounts receivable. Northbound presumably generated over $15 million in sales during 2021. Immediately after the event, HireQuest sold the acquired assets for $6.4 million and the buyers became franchisees.

Northbound was co-founded in 2010 by Greg Feder and Rachel Feder. Both commented at the time of the acquisition they’d continue leading the company and working with Richard. They are still managing partners and have a place on Northbound’s board of directors. Moreover, the whole executive team and other partners remain in their positions. Most of these people have worked at Northbound for several years, with some going back over a decade.

In December of 2022, HireQuest acquired MRI, which was a significant acquisition. MRI had 232 franchise offices, mostly in the US, and had generated $283 million in system sales, which translated into 11.3M in income from royalties and 1.9M in LTM EBITDA. HireQuest recorded 4.9M in goodwill in the transaction.

In December of 2023, HireQuest acquired The Employment Company (TEC), which had ten locations in the Northwest and Central Arkansas, for $9.8 million. TEC was founded in 1979 and reportedly generated $34 million in sales on the trailing twelve months ended in September of 2023. Immediately after the acquisition, the assets were sold for $7.6 million. This led to the conversion of all acquired branches into Snelling franchises.

Conclusively, the peculiarity of turning company-owned locations into franchisee-owned end up very positively impacting the economic cost of M&A. Although the headlines may indicate a certain number, HireQuest has mostly managed to get a great deal of cash out of converting the acquired branches.

It’s fundamental to highlight that Richard seems to only acquire a business when the terms are highly favorable for HireQuest. This is partly the reason why he runs HireQuest on a very healthy balance sheet. Minimizing costs is a further cornerstone of Hermann’s strategy, massively helping in economic down cycles.

“ as it relates to M&A, I'd like to point out that we've been able to maintain a healthy balance sheet and low leverage throughout all these transactions. Since the beginning of 2021, we've increased system-wide sales by just shy of $400 million. We've invested over $75 million in acquisitions and finished 2023 with net debt of $13.4 million. I'll also highlight that fully diluted shares over that time have increased from about 13.7 million to only 13.8 million at the end of 2023. That is, we financed our growth almost exclusively with cash flow from operations.”

Finally, Richard has repeatedly managed to keep the same people who were running the branches before them becoming franchises. This is one of the most crucial aspects of HireQuest’s M&A. Turnover is the most common value destroyer in these types of deals, and Hermanns has consistently managed to execute well above average.

It is impressive how they were able to grow and acquire smaller players, and not have large debt coming with it. Interesting model for sure!! Great read, thank you!