HireQuest is a staffing company, founded in 1991 by Richard Hermanns and Dan McAnnar. It started as an on-demand labor provider for daily-paid jobs. Over the past 3 decades, HireQuest has added long-term placements and executive recruitment services, operating as a network of different brands. Richard currently runs the business and has a 38% stake; a long-time partner, Edward Jackson, owns another 18.7%.

HireQuest has a franchising model, providing them with many advantages over small peers. Firstly, the staffing business requires hiring employees before clients pay for their services, which is a great impediment for small firms. HireQuest funds working capital needs and acquires ownership of customers’ receivables. Secondly, compensation insurance is a big cost for staffing firms. HireQuest centralizes it. Given the company has over 400 branches, it can negotiate much better terms with insurance companies.

Staffing firms with company-owned offices need to hire branch managers and overseers. HireQuest avoids both costs, strongly enhancing margins. In addition to this, the industry is subject to very high turnover and other factors as a byproduct of it being a people business. Having all branches led by their owner greatly aligns incentives, improving execution.

HireQuest went public in 2019 by reverse merger, “acquiring” a then mismanaged public company called Command Center, which had company-owned offices. This is another spot where HQI’s model shines. It shows its aptitude for large integrations and reveals how big of a role incentives play. HireQuest has grown from 100 locations to 400+ mostly via M&A since 2018.

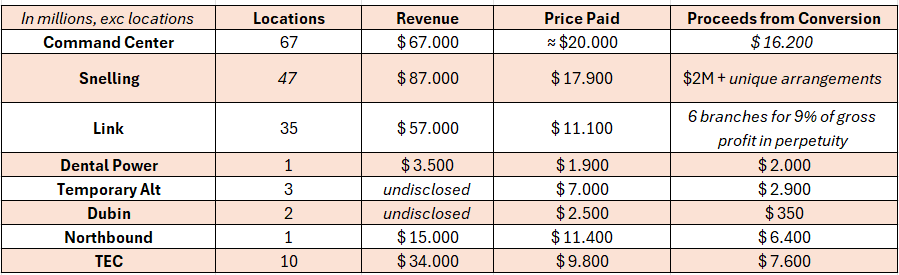

When HireQuest acquires a firm with company-owned offices, they sell them and enter a franchise agreement. After conversions are considered, the price HireQuest ends up paying for the acquired company ends up being much lower than headlines report. These are some of their acquisitions.

The staffing industry, being a people business, makes M&A highly problematic. Branches’ worth is defined by a manager’s capacity to keep the customer list together. Almost always, it’s done so because of the people in charge. Hence, when a staffing company is acquired by one with company-owned offices, managers resign, and the acquired branch might lose over 50% of their revenue. Additionally, turnover is enhanced when this occurs, making acquisitions highly deceptive. HireQuest avoids this issue by keeping the managers in place. It’s mostly them to whom the branches are sold.

HireQuest finds itself in a very advantageous position for M&A. In addition to the aforementioned elements, the staffing industry is highly fragmented. There are many small offices, some family-owned, that dominate niches and local markets. For most staffing players are very large, they don’t compete for these acquisitions. This provides fertile ground for HireQuest to deploy capital at attractive rates of return for a decently long time.

Disclaimer: This is not financial advice.

If you are looking for more information on HireQuest’s current stance, check my equity research and Q3 earnings review.