HireQuest Network and Industry

Comments on numerous topics related to HireQuest's business

Opening of a New Office as a Franchisee

Franchimp is a website that contains information on franchising businesses. More specifically, it has financial metrics about the individual units within different franchising networks. Things such as how much the initial investment is for opening a particular store/office and the legal document that franchisors’ send to prospective franchisees.

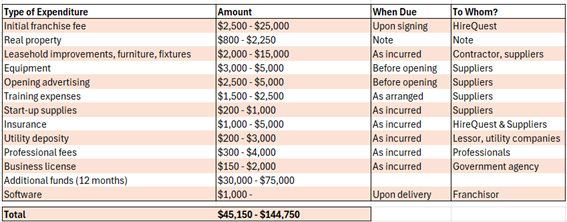

To open a HireQuest or Snelling franchise and offering the different types of services the company has available, a franchisee’s initial investment is estimated to be between $45,150-$145,750. It usually takes 4-12 weeks for a franchise to be opened after the agreement is signed. The investment includes a sum that must be paid upfront to HireQuest, which ranges from $3,500 to $26,000. This encompasses the initial fee that’s between $2,500 and $25,000 depending on the territory wherein the franchise is set to be opened.

The population determines whether the initial fee falls near the higher or lower bound. Territories with over 1 million people require a $25,000 fee, whereas a $2,500 fee is for territories with less than 100,000 people. Although the franchisee is who ultimately decides where to open, HireQuest’s approval is required and the team assist franchisees on the process. Finally, HireQuest generally advises taking on a lease and they are willing to help negotiate with the landlord if the franchisee requests it.

After the person pays for the initial fee, he or she is scheduled to attend training sessions, alongside employees who’ll join them in the endeavor. They attend 2 weeks of training at an operating branch within 30 days before opening their own business. Part of the instructions relate to the usage of software, for which the franchisee has to pay $1,000 upfront.

The following table groups the types of expenditure franchisees need to incur, the amount in dollars, when they are due and to whom.

After the initial fee is paid, HireQuest demands franchisees to pay other fees related to the ongoing operation as well as to punish for delays or negligence. In addition to the royalty fee, which is a percentage of gross billings or funded payroll, these are the other fees I found relevant to franchisees.

Finally, there are two things I’d like to highlight. Firstly, HireQuest mentions the possibility of them financing up to $25,000 of a franchisee’s investment, though, in rare instances, HireQuest could provide up to $100,000. Secondly, the company generally agrees with franchisees to a minimum performance standard in HireQuest Direct franchises. If franchisees do not meet their minimum yearly target, they have to pay the fee they would have paid should they’ve met the standard.

Franchises Network

When HireQuest was a private company, in 2017, the company had a total of 79 franchised locations. After the merger and integration of Command Center, rapid growth followed in the network’s store count. By mid-2024, HireQuest had 414 stores.

The following chart illustrates the number of stores opened, closed, and acquired by HireQuest for the period 2018-2024. Over the period, most of the company’s growth came from acquisitions. By this means, HireQuest added 331 franchised locations to its network, before accounting for subsequent closures thereof. Stores opened during these 6 years amounted to 89, whereas 85 franchises were closed. Of the total, 53 closures occurred in 2023 and the first semester of 2024, combined. I suspect most of discontinued branches were from acquisitions made, with MRI being the network that probably experienced the largest number of closures.

It is worth reminding the reader that HireQuest’s franchisees might operate 1 or more franchises. Therefore, the closure of a location does not necessarily imply the loss of all the revenue generated by that branch. Operators with 2 franchises might choose to discontinue one operation but keep servicing part of the customers with the continued location.

“Of these closures, 11 were in metropolitan areas where our franchisees still maintain at least one office that we expect can service customers of the closed or consolidated offices” Q2 21 10Q

Turnover and losing the customer list are the most severe threats when acquiring a franchising business. It is remarkable to observe how many of the acquired branches end up continuing operations. Based on Hermann’s general commentaries, it’d be expected to lose a high percentage of each location’s business when it’s acquired, maybe exceeding 50%. In addition to this, employee turnover, if not managed appropriately, can destroy a franchising business. It is therefore very interesting to observe how many of the acquired franchises remain open, validating Hermann’s statements.

The fact that HireQuest can acquire networks whose size is very large relative to their own speaks well about the smooth integration process. In 2019, HireQuest essentially acquired Command Center, which had a size of almost 70% that of HireQuest. Thereafter, Link and Snelling implied the acquisition of a network 50% of HireQuest’s size. In 2022, HireQuest acquired MRI, which had over 200 franchised locations, while HireQuest had around that number as well.

Notwithstanding this, acquisitions blurry the picture as to how satisfied franchisees are, for it clouds the renewal rate, which, incidentally, is not reported. I suspect that, prior to the merger, and naturally thereafter, the HireQuest Direct network has had the most satisfied franchisee base, which led to a high renewal rate. Consistent growth with no severe declines and numerous franchisees owning more than 1 branch make me think the latter might be true.

When the merger took place, many franchisees signed 5-year agreements, causing multiple renewals to be scheduled for 2024. Furthermore, when HireQuest acquired MRI, dozens of franchise agreements were discussed and rearranged. Many of MRI’s franchisees opted to have their scheduled renewal in 2024. This is something that happened with other acquisitions, though to a lesser extent. HireQuest entered 2024 with 83 renewals to be signed in the course of the year. By August, 24 offices had been closed. Depending on the dates at which these renewals are scheduled, the corresponding renewal rate.

System-Wide Sales

Prior to merging with Command Center, HireQuest had system-wide sales of $190 million. In the last fiscal year, ended in December of 2023, the company reported $605M in system-wide sales.

It’s important to note that, whereas store count increased by over 340% during the period 2018-2024, system-wide sales increased 218%. This entails that the average sales per HireQuest location, including all trademarks, have fallen quite severely. Before the merger with Command Center, each branch generated 1.95M dollars in topline, on average. During 2023, each location generated, on average, $1.4M.

Note: The chart is made by dividing system-wide sales by year-end store count.

Note: 2022’s year-end store count includes MRI’s, but not their revenue during that year, for it was acquired in the last quarter.

The following chart computes system-wide sales per HireQuest brand, and thereby business model, for the three largest contributors. Although the company shares system-sales per brand on a quarterly basis, fourth quarters are not separately disclosed. Therefore, the fourth quarter of all years are estimations.

Part of management’s strategy revolves around leveraging their large and growing network of franchises and increase offerings. Some can be offered by existing branches, whereas others may take specifically dedicated locations. HireQuest bought Dental Power’s staffing division to launch their health platform; it launched TradeCorp for highly specialized labor in the construction industry; and DriverQuest for long-haul rides. Their impact on system sales remains negligible, but nonetheless growing, especially DriverQuest and TradeCorp, which I suspect don’t require dedicated locations for them to be offered.

Followed from system-sales each brand contributes, we can observe that, during 2023, 41% of the total was generated by HireQuest Direct network. This is done while HireQuest Direct offices might represent around 30% of HireQuest’s total network. Snelling and HireQuest contributed 26% of total system-sales, and the executive and permanent placement franchises generated 31% of total.

Royalty Fees

Different brands not only carry distinguished offerings, but some aim at significantly different end markets and differ in business model. HireQuest Direct does direct dispatch and focuses on daily-pay jobs in the construction and light industrial segments. This implies a cost structure and day-to-day operation that differs from HireQuest and Snelling locations, which are focused on longer-term positions in the administrative and light industrial markets. MRI offers permanent placement services and, Nortbound, executive placement. Both aim at different markets, the method by which they earn revenue is different than that of daily labor offerings and carry different margins. Therefore, to the extent that it is possible, each business unit’s royalty fee will be separately assessed.

Low data availability impedes me from finding and computing charts illustrating accurate figures. Apart from HireQuest Direct, other brands include a large degree of estimation.

HireQuest Direct

HireQuest Direct is distinct from the rest of brands in that acquired locations are rarely added to their network. I suspect that direct dispatch, being a rather unique feature in the staffing industry, turns HireQuest Direct into the most difficult franchise to grow inorganically. My speculation partly lies on the fact of how slowly this franchise – formerly known as Trojan Labor – had grown until 2019, compared to other units in the recent past.

HireQuest Direct generated over 90% of the company’s royalty income in 2019, suggesting that almost the completeness of the franchising network was made of HireQuest Direct offices. This translates into over 120 offices at that time, which reportedly increased to 131 by mid-2024.

Royalties generated by HireQuest Direct have thus remained relatively flat, with the implied fee over system sales varying. Having averaged 6.2% and considering the fee structure of decreasing fees per incremental million in sales, it’s plausible to think that the average HireQuest Direct location generates over $2 million in topline. This would be in line with the estimated average location’s revenue prior to the merger in 2019.

In the franchise agreement document, HireQuest disclosed the average and median gross profit and net profit for HireQuest Direct offices. Topline was not disclosed, for which margin calculation cannot be performed. Notwithstanding this, it’s fair to speculate that these offices may operate with a net profit margin of at least 10%, on average.

HireQuest Health

HireQuest acquired Dental Power’s staffing division in late 2021, but the company reported over $200,000 in income from fees for that year. It remained company-owned for some time and was sold in March of 2023 to an MRI franchisee for $2 million, payable over 5 years.

Since the time of the acquisition until mid-2024, HireQuest earned over $1.1 million in accumulated royalties from their health division. The percentage fee charged to the operation, prior to the franchisee joining, is obscured by disclosed data. After Q2 of 2023, I’d estimate the fee to have been around 6% of system sales.

Note: Q4 of 2022 and 2023 are estimates

As time goes by, quarterly reports will shed further light on this business unit, but my suspicion is that capital was fantastically deployed in acquiring Dental Power’s staffing division. Richard bought it for $1.9M in December of 2021, sold it for $2M in March of 2023, and generated 1.15M in royalties throughout late 2021 until mid 2024.

Snelling and HireQuest

Snelling and HireQuest represent the more classical staffing offices HireQuest has. Although they were reported separately for most quarters, throughout 2022 and 2023, management included all acquisitions’ royalties alongside these two. In consequence, the following chart plots my estimated royalty fees throughout this period.

It’s notorious how Snelling’s acquisition virtually created this business unit for HireQuest. Since inception, Richard had mostly focused in the direct dispatch model for daily jobs. Nonetheless, most of the industry’s offerings align better with Snelling’s business, for which new M&A is most likely to be added to their network. Snelling’s brand is a very valuable asset, and management will be extracting its juice accordingly.

MRI

MRI’s income from royalties is reported to have been $7.8M during 2023, whereas total system wide sales were not disclosed separately. Notwithstanding this, I’d estimate MRI had system sales of $180-$200M, implying MRINetwork lost around $80-$100M in system sales. Part could be attributed to offices closing due to the acquisition, but another part is due to the cyclical downturn the industry experienced, which continued throughout 2024.

The following chart reports MRI’s 2023 royalty income. During 2024, management did not disclose MRI separately, but they included it alongside Northbound and SearchPath. This partly makes sense since they share business model and, to some extent, end markets. These businesses generated $1.65M in royalties during the first quarter of 2024 and $1.74M in the second, representing a 4.3% and 4.2% of system sales, respectively.

Some Industry Considerations

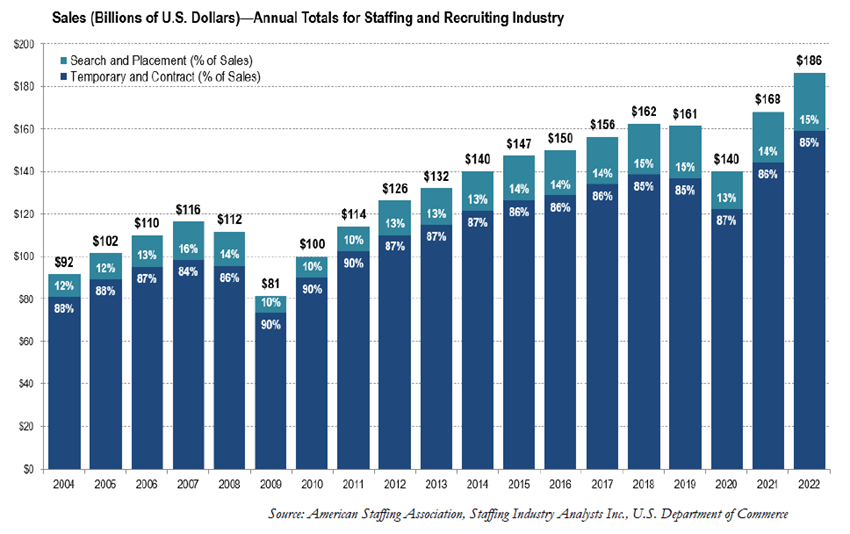

The staffing industry has been around for numerous decades. In fact, the service is so fundamental and simple that it probably goes back further back. A more systematic approach to fulfilling this business need probably emerged as a consequence of economic growth. The American Staffing Association estimates that sales for the staffing and recruiting industry have grown from $92 billion in 2004 to $186 billion in 2022, exhibiting a 4% CAGR.

A further interesting point relates to the sources of sales. Broadly speaking, the industry is separated into search and permanent placement, both for employees and executives, and temporary labor and contract, where the services provided are on a per-day or week basis. To some extent, over the past two decades, more emphasis has been placed on working on a per-project basis. Having said this, ASA estimates that temporary services have systematically generated most of the industry’s revenue.

The industry is highly cyclical, greatly tracking the US economy. When businesses expect demand to increase, mostly catalyzed by a recent increase thereof, they adjust supply accordingly, hiring people beforehand. When tides turn, it’s not always the case that companies will lay off employees, but they will at least pause hiring. Under such circumstances, staffing companies’ revenue declines, for their services are not required. Although Robert Half is focused on financial services’ and administrative positions, I believe their quarterly revenue chart very well illustrates the industry’s cyclicality.

A large part of HireQuest’s business, and the industry for that matter, revolves around providing temporary services to construction companies. Being the latter very sensitive to economic cycles, as capital available for investments expands or contracts, staffing businesses tend to follow the same pattern. More specifically, HireQuest Direct, which focuses on daily paid jobs, will immediately suffer as projects are paused.

Moreover, staffing businesses’ margins tend to follow a cyclical pattern as well. A business that operates a model of company-owned offices has a relatively large component of fixed costs. They cannot stop paying for many operating expenses, such as the lease of a building or floor. Furthermore, since employees are hired before a client effectively solicits their services, payroll has to be temporarily incurred before adjusting to the new situation and hiring less people.

Despite the latter being mostly the case for staffing companies, HireQuest’s royalty model partly insulates them from cyclical margin contraction. The company earns either a percentage of gross billings or of funded payroll, independent of the gross margin franchisees may earn during a certain period. Therefore, even if franchisees might experience a contraction in margins, the downside HireQuest can experience is capped.

As a consequence of the industry’s cyclicality and its implications, the number of competitors tends to increase as economies grow and they diminish when economies contract. Incidentally, this largely contributes to creating fertile soil for Hermann’s M&A strategy. When staffing businesses struggle, HireQuest’s world of potential acquirees increases.

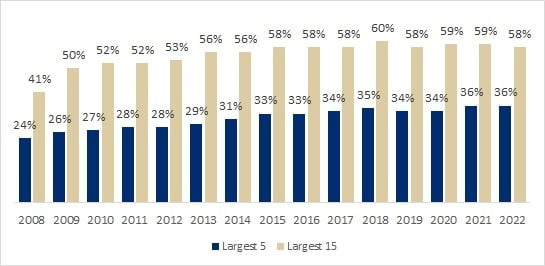

This is something that, throughout the years, has manifested itself on a broad basis within the staffing industry. The following chart, illustrating the percentage of business that’s captured by the largest 5 and 15 companies, suggests the industry has been tending towards consolidation.

My suspicion is that this trend will continue. However, it must be observed that most local and small markets are dominated by old firms, who keep the customer list together. If a business that runs a company-owned office model acquires one of these, it’s very much likely that they will lose a big percentage of the branch sales due to turnover and customers leaving. HireQuest is less likely to experience such a decline, for the same people that were running the branch tend to stay after the office is added to HireQuest’s network. It’s important to note that this fundamental aspect of the staffing business can potentially cause temporary sales to decline severely.

“You might have a big project that's ending. You might have an H.R. manager that quits, and you lose your third largest account. And you may be lucky to get 80 percent of your prior year sales, but it's understanding those types of things.”

The industry consolidation has a further positive side effect for HireQuest. As leaders get larger, their incentive to pursue small acquisitions decays. The high fragmentation, with many family-run businesses who may have 1-5 branches, causes a relatively large part of the industry to be of no interest to large players. This part of the market creates perfect conditions for HireQuest to continue growing through M&A with no competition for their deals.

The Staffing Industry and Unemployment

Historically, the demand for staffing services tends to increase as unemployment rates decrease. The latter implies a reduction in the pool of people you can potentially hire, and I suspect it’s further aggravated by the fact that good employees tend to be hired first. In these situations, a hiring company would need to incur substantial operating expenses to do the diligence and interviewing process. Hence the value proposition of a staffing firm that provides permanent placement or temporary labor massively increases.

The obverse is the case as well. The unemployment rate increasing not only damages the staffing firms’ topline because their services are in less demand, but the cost of hiring decreases. There is a further problem that, when the economy contracts, the reduction in potential clients incites stronger competition between staffing firms. On occasions, this can lead to pricing pressures, hitting margins.

Management suspects that, although growth for staffing services have outpaced overall economic and employment growth, there is a fundamental element that will continue to drive industry growth. Hiring is getting increasingly expensive, and the benefits of contingent workers are starting to be noticed by executives. Eliminating the need for looking for someone and running the interviewing process as well as compensation insurance avoids incurring extra expenses while still getting the activity done. Furthermore, the associated flexibility is highly desired if a business wants to expand or contract according to their true needs. Flexibility ends up enhancing efficiency.