Grew 4x in past 4ys - trading at ~2.5x EV/FCF

IPO'd last year - likely overlooked by the market

Highlights:

~$200M mkt cap; $80M EV.

~2.5x EV/FCF.

20%+ operating margins; profitable (at varying degrees) for past 5 years.

Singaporean company; O&G industry.

A few years ago, How Meng Hock was leading OMS when Sumitomo (former parent) wanted to liquidate it due to the o&g down cycle. How Meng bought the division from them for $2mm in late 2023. He turned OMS around, secured an estimated $120-$200mm per annum deal with Saudi Aramco, and listed OMSE in the Nasdaq at a ~$350mm mkt cap. How Meng didn’t sell a single share out of his ~60% ownership, despite the extraordinary results of his investment.

What OMS Energy does

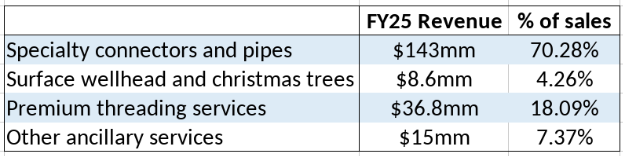

OMS operates in the O&G sector, selling to onshore and offshore exploration and production companies. They manufacture surface wellhead systems and specialty connectors and pipes. Because customers’ wells are in tough environments, OMS needs to meet specific requirements on temperature, corrosion, pressure. In addition, OMS sells premium threading and other ancillary services.

Customers include Chevron, Saudi Aramco, Halliburton, Baker Hughes, Weatherford.

Saudi Aramco (67% of FY25 revenue)

OMS entered into a 10-year supply agreement with Saudi Aramco in Jan 2024. Management estimates it represents a potential $120-$200mm per year, though Aramco has no obligation to purchase any minimum amount and they can terminate for convinience. Customer concentration encompasses the largest risk OMS faces.

However, I’ve reasons to believe the contract is doing fine and might even expand.

OMS mostly sells specialty connectors & pipes to Aramco. In the first half of FY26, revenue from this source was $51mm, and OMS announced an $11mm call-off order in March. The deal is at least ongoing.

To some customers, OMS sells the connectors & pipes and leverages that to further sell their after-market services. They couldn’t do this with Aramco because OMS didn’t have the industry certification for some of these. But in the same press release where they announced the $11mm order, management hinted OMS Saudi can now provide repair and maintenance services for wellheads and christmas trees. This is after they earned the API Specification 6A certification in January 2026. It’s always easier to select just one vendor.

Manufacturing Sites

The second reason why I suspect their contract with Aramco might expand is because of OMS Energy’s strategic footprint. Over the past decade, regulation has been tilting towards favoring local manufacturers; in certain countries, you can’t even bid if you don’t manufacture locally and employ local people. Saudi Arabia is an example thereof, as well as Indonesia. OMS has local presence in both locations and is thus favored when compared to most competitors. In addition, the company owns manufacturing sites in 4 other jurisdictions.

Financials – H1 Results

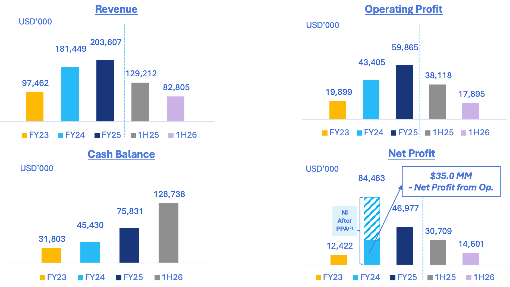

The company grew from a ~$50mm run-rate to $200M in the span of three years, mostly attributed to Aramco. Operating profit rose faster as fixed costs were spread across more units.

In the first half of FY26, revenue decreased 36% and margins contracted highly, but the operating margin was 21.6%. Though bound to experience volatilility, OMS Energy has a decent profit margin baseline.

Trend of Economics and Cash-generation Capacity

Sales decrease in H1 were due to the overlapping of two contracts for Aramco and unusually high call-off orders last year. Revenue from pipes & connectors contracted by 46%, whereas the rest of the business fell by 5% YoY. When this happens, and further reducing customer concentration risk, OMS benefits from a healthier mix. Pipes & connectors carry ~23-31% gross margins; SWS & Christmas trees ~24-30%; premium threading ~28-39%; and other ancillary services ~42-47%.

Most of OMS’s business, ex-Aramco, is centered around the higher-margin products. The 2nd large contract they have is with Halliburton, which I estimate generates ~$15M/yr in sales of premium threading services. Even in places where they do sell pipes, connectors, and wellheads, OMS tries to upsell customers and increase contracts’ average margin.

In addition, despite having ~$30M in 11 manufacturing sites, OMS needs minimal CapEx for maintenance. The company is thus able to generates large amounts of free cash flow: $27.9M in FY23; $16.7M in FY24; $37.6M in FY25; and $25.7M in first half of FY26.

Inventory-building and destocking is the primary driver behind cash-conversion dynamics.

IPO was for branding and expansion

Though many businesses get listed because they need capital, OMS Energy does not. How Meng Hock mentioned the decision was made to drive awareness and branding. In fact, SG&A barely increased from $4.9M in first half FY25 to $5.4M in first half FY26. I suspect this is due to the annual legal and auditing costs required to be listed in the Nasdaq; not to headcount growth.

They want to get better known globally and are hoarding cash waiting for a good M&A opportunity. It’s likely that OMS follows a tuck-in model, to expand portfolio or add geographies, instead of acquiring for manufacturing capacity. To the effect of branding, management is doing some IR efforts; How Meng attended a conf in CA and will be in Planet MicroCap’s in June.

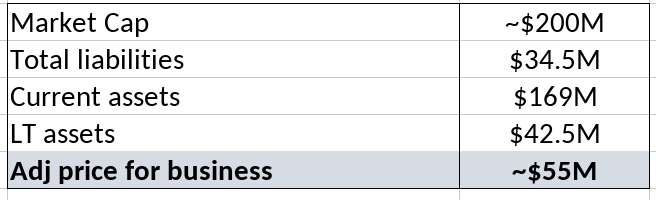

Estimation of the true price OMS trades at

The company’s EV and mkt cap suggest a $120M net cash position. However, this severely understates the balance sheet’s health. A closer look point to a significantly lower price the business currently trades at.

Reminder that OMS generated $17.8M in operating profit over the first six months of FY26, $14.6M in earnings, and $25.7M in free cash flow.

Final Remarks

Out of $203M in FY ‘25 sales, $136M originated from Saudi Aramco. Management mentioned FY25 included unusually large call-off orders, for which I suspect a normal run-rate hovers ~$160M in total sales. Strip out Aramco’s 67% and we’re left with a business that has $52.8M in revenue, mainly focused in the higher margin products. Likely, it’d still be capable of generating ~$10M in cash per annum. At this valuation, it’s trading at ~5x that. Furthermore, given their FY has ended but hasn’t been’t reported yet, it’s likely that their valuation is getting compressed a further 1-3x. Profit generated is acting like accrued interest in bond coupons.

Disclosure: This is not a recommendation to buy or sell any security. I must nonetheless disclose that I own a position in some of the securitie(s) discussed. In addition, the foregoing write-up is just the result of my dd and opinion. Please do your own research.