I’m catching up with earnings write-ups. In the next couple of weeks, I’ll be publishing my reviews on Texas Instruments, Visa, Zoetis and Mercado Libre. It is my intention to have them as soon as possible, though I’ve been heavily time-constrained these past months.

Overall Financial Analysis

Alphabet reported third quarter results on October 24th. The company had revenues of 76.69bn, growing 11% on a yearly basis and slightly sequentially. Ever since last year’s fourth quarter, sales growth has been accelerating noticeably. For the 4Q22, 1Q22, 2Q23 and 3Q23, revenue grew 1%, 3%, 7% and 11% respectively.

The pandemic strongly increased web traffic demand, fueling Google’s advertising services. As is normally the case, a large part of this extra demand was simply pulled forward in time, for which periods of growth digestion are natural. It is worth stating these can last quarters or even years. In any case, a continuous uptrend would imply the “digestion period” is over for Alphabet.

Alphabet posted record gross profit, which came in at 43.6bn for the quarter. The gross profit margin was 56.7%, down sequentially, but up 280bps yearly. Operating income for the company was 21.34bn, operating at a 27.8% margin, up from 24.8% last year. Lastly, Google generated 19.68bn in net income, meaning Alphabet had a 25.7% net profit margin. The latter expanded 560bps YoY and 110bps sequentially. I’d like to point out that a yearly comparison is somewhat flawed as Google’s third and fourth quarters of 2022 were weak compared to these past 3 years average.

At the end of last year and also the beginning of this one, management had called for cost-discipline measures. They mentioned and emphasized their intention of returning Google to its previous levels of profitability by a complete re-engineering of the cost structure. One of the big decisions the company made was to not only stop hiring, but doing layoffs. At an average salary of 250k (arbitrary number), every 10k employees that are laid off, the company gets to save 2.5bn in opex. This past quarter, headcount grew only slightly QoQ.

Turning into the cash flow statement, Google brought in a record 30.65bn in cash from operating activities, up from 23.3bn last year. On the other hand, capital expenditures were 8.05bn for the quarter. This leaves free cash flow at 22.6bn, the highest the company has generated in a single quarter. The free cash flow margin stood at 29%.

Breakdown by Segment

Before going into it, I always find this image useful for remembering where are business units included.

Google Services

Google Services is the most relevant contributor to Alphabet’s toplin and generated 67.98bn dollars in the third quarter. The segment grew 10.7% YoY and represented 88% of Alphabet’s total sales, with the latter being the case, on average, for the past time. Furthermore, it did 23.93bn in operating income, implying a margin of 35.2%, which expanded 300bps YoY.

Diving further,Google Services is composed of a wide array of products and services, which are grouped under two large labels: Google Advertising and Google Other.

Google Advertising

This segment consists of GSearch & Other, YouTube ads and Google Network. I’ll go over each of these, but, starting with Google Search & Other, it generated 44.02bn in revenue, up 11% on a yearly basis and 3% QoQ.

During 2020/21, GSearch & Other’s size basically doubled, with growth rates reaching 50%+ at 100bn+ run rate, surreal. Companies that experience this kind of unusually excessive demand generally tend to contract in the following years, as it is like the business has got a few years ahead of itself.

Nonetheless, even though revenue growth decelerated, it kept growing in all quarters with the exception of Q4 of 2022, when it declined 1%. After that period, revenue accelerated to 1.8% in Q1, 4.8% in Q2, and 11.3% in this one. This should help illustrate GSearch’s resilience. TTM revenue stands at 165bn, high levels of growth should not be expected moving forward.

Google Network is composed of Google AdMob, AdSense and Ad Manager. GNetwork’s revenue declined once again on a yearly basis, this time being 2.7% down and generating 7.66bn. Alike GSearch and almost all ad-companies, this business unit saw abnormal growth during 2020-22 for which digestion is expected and natural. It is worth reminding that management said in some calls that the recovery in Network had been slow.

It is unclear to me why is GNetwork struggling much more than Google’s other businesses. Could be a product of how competitive the ad landscape has become with Apple, Microsoft and Amazon flooding the space. It is my view, though, that comparisons with Search are off. GSearch is one of the best products/businesses that have ever existed.

YouTube, moving forward, generated 7.95bn in revenue from advertisements during the third quarter of 2023, growing 12.4% on a yearly basis. After a period of perceived stagnation by the market, the platform is very quickly ramping up, once again. YouTube has been facing several headwinds for the past couple of quarters which basically consist of growth digestion, YouTube Shorts and Subscriptions. It’s still early to tell, but definitely trending in the right direction.

As a sidenote, YouTube’s “controversial weakness during 2022-23” is a perfect example of how generally disconnected are the financial community’s narratives and the business fundamentals. It is worth noting as well that, if YouTube reported its subscription revenues alongside ads, I suspect the chart would show much more resilience and pronounced growth.

Google Other is the final component of Google Services. It is composed of, mainly, Google Play Store, YouTube subscription offerings and hardware sales. Google Other brought in 8.33bn in revenue during the quarter, increasing 21% YoY and surpassing YouTube ads and GNetwork’s contribution to Alphabet’s topline.

Even though the name of this segment makes one think it is trivial, YT subscriptions and Play Store are expected to continue driving high growth moving forward, alongside, I think, higher margins. Additionally, the Pixel phone has been gaining traction these past quarters and is estimated to continue doing so, given the launching of the new version, which includes generative AI capabilities.

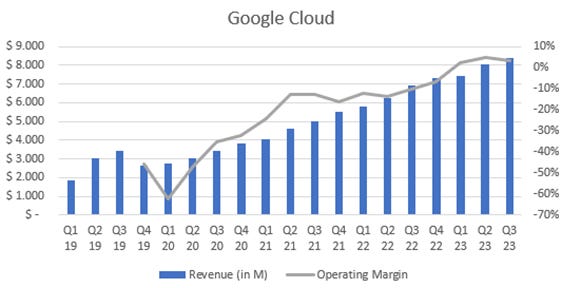

Google Cloud

In here, we have two products: Google Cloud Platform (GCP) and Google Workspace. Google Cloud has grown at an extremely fast pace for the past decade, but the problem had always been its lack of profitability. The more quarters went by, the more money was lost.

In the first quarter of 2023, the segment turned operatively profitable for the first time and the trend continued throughout the year. GCloud generated 8.41bn in revenue, growing 22% on a yearly basis and 4.7% sequentially. Operating income for the segment was 266M, implying a margin of 3.1%. The latter declined from last quarter’s 4.9%, but expanded 1320bps on a yearly basis.

Google Cloud had been holding its high growth rates, allowing it to take some of the overall market share from the cloud computing space. However, this is the first quarter when growth highly decelerated and much more than Azure. The latter continues to excel. Amazon Web Services, on the other hand, kept hovering the 12% growth rate which, at its size, is nothing but impressive.

Management Commentary and Outlook

Management started by pointing out that the business is doing phenomenally, overall. Most business units have been gaining traction once again, while yearly growth pronouncedly ticked upwards. In general, this is due to a lighter advertising landscape, AI enhancements that were able to drive products’ value further, YouTube’s momentum and recoveries across other businesses like Play and hardware sales.

A lot of emphasis was placed on Alphabet’s horizontal offerings and how AI integrations across the board have been creating enormous value for users. The team is experimenting to bring more AI features to Search, Bard has been successfully integrated with other of Google’s products (Gmail, Maps, YT, etc) and advertisement offerings keep delivering higher ROI for customers. Finally, Duet AI (Microsoft’s Copilot competitor) testing continued during this quarter and management keeps expanding its capabilities and platform reach, including Cloud products, services, and Workspace. As a sidenote, the latter surpassed 10M paying customers, up from allegedly 9M in the previous quarter.

Secondly, management is extremely excited about YouTube. They have recurrently mentioned throughout all quarters how the platform is positioned to capture immense growth ahead. YouTube had been facing a couple of headwinds for the past two years, with a relevant one being Shorts. When launched, the product was not optimized for monetization nor did the team want to drive it, since, at first, one wants to aim for high usage and consolidate network effects. This quarter, management mentioned once again that monetization has been improving in Shorts, partially closing the gap and helping YouTube’s topline. Furthermore, management the following:

“Shorts now average over 70 billion daily views and are watched by over 2 billion signed-in users every month.” (Up from 1.5bn MAUs and 30bn daily views last year)

Turning to cloud, which is always the third pillar for commentary, not much concern was perceived considering the high deceleration the business saw. Management stressed that this was mostly due to customers’ optimizations efforts with regards to their spending. Nevertheless, Google Cloud is still a top choice for businesses and mostly in the AI space.

“Today, more than 60% of the world’s thousand-largest companies are Google Cloud customers.”

“We offer advanced AI-optimized infrastructure to train and serve models at scale, and today, more than half of all funded generative AI startups are Google Cloud customers.”

“From Q2 to Q3, the number of active generative AI projects on Vertex AI grew by 7X”

Finally, in the first quarter of 2023, management started mentioning their strong intention of optimizing Alphabet’s cost structure. The message was reiterated throughout the year and was backed by some initiatives. Moving forward, they plan to continue reassessing their real estate footprint and usage, slowing down the pace of headcount growth while talent is reallocated to top priority areas and, overall, improving all of Alphabet businesses’ productivity. This is expected to continue translating into higher revenue growth than expenses’. Capital expenditure, on the other hand, is completely destined towards servers and building cloud infrastructure, which should lead to an improved offering for customers and an ever-expanding reach.

My Take

Alphabet had the best quarter of the past year in my view. It is always important to try to attach to facts rather than opinions and make one’s own mind of things. The companies’ products, mostly Search and YouTube, saw an indescribable amount of negative attention, which could have clouded judgement. Nevertheless, quarters go by, and all businesses keep proving there’s still a long runway ahead, alongside profitability.

Regarding cloud, I see no real concern in experiencing some QoQ decelerations, even if dramatic. Not only is deceleration expected as scale is gained, but it’s also natural. As with investment results and most trajectories, business’ growth is not linear. The operating leverage this business unit experienced for the past years is nothing but impressive, while it also kept delivering on topline. Time will tell if this deceleration means something else, but there’s little to make out of it with only one quarter of data.

Finally, what I want to address is that, in my view, Google is neither Search, nor Cloud, nor any specific business. I find Alphabet’s best description to be a conglomerate of different business units, all of which still have a long runway ahead. Even if one of these start to decelerate, the others should continue fueling Alphabet forward.

I will leave you with an interesting extract of what I consider to be the still most underrated business Alphabet has. It is unfathomable how strong YouTube’s network effects are and how its structure should continue allowing it to tap into multiple audiovisual verticals:

“Let’s shift to YouTube. It’s worth repeating: our intense focus on creator success coupled with our multiformat strategy are at the center of how we think about YouTube’s long-term growth. Shorts, Connected TV and our subscription offerings are key drivers here, and we’re investing across each to solidify YouTube’s position as the best place to create, the best place to watch and the best place to deliver results.”

Personal Commentary

I will try to continue catching up with earnings reviews in the coming weeks. Hope you found this one useful!

Contact: giulianomana@0to1stockmarket.com

Thanks for another amazing read my friend !

Great job mate!