Alphabet reported their first quarter results earlier this week. I think the best way to approach companies that cover a lot of ground is to split the article into two parts. The first one will consist of an overall financial analysis of how the company as a whole performed. In the second part, we’ll go through each business unit in a bit more detail.

Overall financial analysis

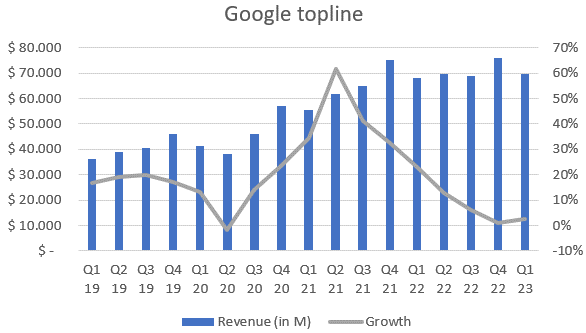

Google reported total revenue of 69.8bn, up 3% year over year, with management pointing out the resilience in search and the momentum in cloud. On a sequential basis, revenue declined 8%, but it always happens in the transition from the fourth to the first quarter, it’s seasonality.

In the first quarter of 2023, Google generated 39.17bn in gross profit, implying it operated at a 56.1% gross margin, down slightly on a yearly basis and up 260bps QoQ. Operating income was 17.4bn for the quarter, with an operating margin of 25%, declining 450bps YoY and up 110bps sequentially. Lastly, net profit margin stood at 21.6%, meaning the company produced 15bn in net income, down 9% year over year.

Moving forward, Google brought in 23.5bn in cash from operations, very in line with the previous quarters and still below the 2021 highs. Capital expenditures were 6.28bn for the quarter. This leaves Google’s free cash flow at 17.2bn, implying the company’s fcf margin was 24.6%, up from 22.5% last year and improving 360bps sequentially.

On the subject, management said they expect CapEx to be higher in 2023 than in 2022, taking a modest step-up in the second quarter and continue throughout the year.

Before going into each business unit, a brief overview. As a whole, Alphabet generated 69bn dollars in revenue. Advertisement revenues were 54.5bn, down year over year, and representing 78% of total revenues. The following charts illustrates how much revenue did businesses contribute as a % of the total.

Break down by segment

If you are not really sure on how are the different segments composed, this image should prove useful.

Google Services

Google Services is the most relevant contributor to Alphabet’s topline, accounting for 61.9bn dollars. The segment grew 1% YoY and represented 88% of total revenue, down from a 90% share last year. Moreover, it is composed of a wide array of products and services, which are grouped under two large lablels, advertising, and other.

Google Advertising consists of GSearch & Other, YouTube ads and Google Network. Google Search & Other generated 40.35bn in revenue, growing 1.8% year over year and declining sequentially, as it does every first quarter. GSearch has continuously proven itself as a truly resilient business unit.

During 2020/21, its size basically doubled. As observed with many companies, those who experienced outsized demand have to, in most cases, go through a period of growth digestions because a large part of this demand was supposed to come later. What is notorious in this segment is that it only declined one quarter and by 1.6% (last one). This is remarkable given the pullbacks many other businesses saw and, again, shows this particular segment’s resilience. Finally, Google Search & Other is now a 160bn business, deceleration is natural.

As a quick reminder, Google Network is composed of Google AdMob, AdSense and Ad Manager. GNetwork’s revenue declined 8.3% year over year, being 7.5bn for the first quarter of 2023. Alike GSearch, this business unit saw abnormal growth rates during 2020 and 2021, digestion is needed. The thing now is when will the period of digestion end. It would be extremely positive to see Google Network reaccelerating moving forward.

Management mentioned that in Google Network there was an incremental pullback in advertiser spend.

YouTube generated 6.7bn in revenue from advertisements, declining 3% year over year. The platform has been a very controversial topic due to its ‘weakness’. In this regard, there are several points I’d like to go over that could offer more context on the reasons behind it:

YouTube Shorts was released globally in July 2021. Management has been heavily focused on its growth and are just now turning their attention to monetization. This creates a headwind in viewership for YouTube long-form videos and, therefore, to their monetization as well.

YouTube began their subscription offerings in 2014, but it is just now taking off. As of the last data I recall, it had over 80M premium subs and over 5M TV subs. This revenue is not included in YouTube ads and, of course, it creates another headwind. YT subscriptions literally eliminate ads from your videos.

The platform also saw abnormally high growth during the pandemic and has been trying to digest this growth thereafter.

Management commentary on YouTube (ex subscriptions):

“Last year, the number of channels that uploaded to Shorts daily grew over 80%.”

“In YouTube, we saw signs of stabilization in ad spend on a sequential basis”

“People are engaging and converting on ads across Shorts at increasing rates”

“YouTube ROI is 40% higher than Linear TV and 34% higher than All Other Online Video”

“Now more than 100,000 creators, artists and brands have connected their own stores to their YouTube channels to sell their products”

Those are the three components of Google advertising services. Altogether, they generated 54.5bn in revenue, slightly down YoY.

Moving forward, the other category that conforms part of Google Services is ‘Google Other’. In here, the two most relevant products the company includes are YouTube subscriptions and revenue generated via Google Play. Google Other brought in 7.4bn dollars in revenue, growing 8.8% on a yearly basis. Management commented that YouTube subscriptions were leading this growth.

All of these leaves Google Services revenue at 61.9bn dollars, up 1% year over year. Furthermore, Services produced 21.7bn in operating income, meaning the business operated at a 35% margin. The latter was down 200bps YoY and up 400bps QoQ.

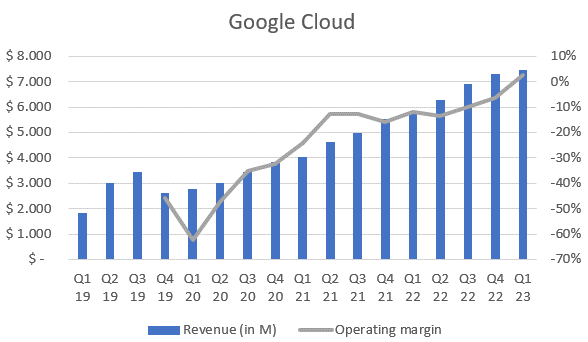

Google Cloud

In here we have two products: Google Cloud Platform and Google Workspace. Google Cloud has grown very rapidly for the past decade, but there was an issue with its profit, it never showed. This changed in the past quarter, as Google Cloud turned EBIT positive. The business unit generated 7.4bn in revenue, growing 28% year over year and 2% sequentially. GCloud brought in 191M in operating income, at a margin that has been continuously improving for the past years. The operating margin stood at 3% for the quarter, up from -12% in the comparable Q and up 1000bps sequentially.

There has been extremely tough competition in the cloud computing space. GCP has been growing rapidly but barely outgrowing Azure for the past quarters. Google Cloud Platform has been retaining its market share and Azure has been continuously gaining more.

Management commentary:

“Over the past three years, GCP’s annual deal volume has grown nearly 500%, with large deals over $250 million, growing more than 300%. Nearly 60% of the world’s 1,000 largest companies are Google Cloud customer”

“Over the last four years, the number of Google Cloud partner certified practitioners around the world has increased more than 15 times”

“Our Cloud cybersecurity products help protect over 30,000 companies”

“Google Workspace’s strong results were driven by increases in both seats and average revenue per seat.” (I think this is like the 7th quarter in a row they say this)

Management commentary and outlook

Alphabet’s management team does not give authentic outlook. The only thing they mentioned is how current trends are going. On ad spend, there was a stabilization in YouTube, resilience in Search and a continued pullback in Network. Regarding cloud, they are pleased with the momentum the business has had for the past quarters and years. Nonetheless, they did say customers are really looking to optimize their costs given the macroclimate, something we also heard in the previous quarter from hyperscalers.

Two more broad topics were covered. On the one side, AI was all over the place. Management reaffirmed Google is a leading company in AI and remembered analysts that integrations have been ongoing in their ecosystem for years now. Concretely, they referred to Bard and said iteration will come, and they released their PaLM API and MakerSuite tool for developers. They also mentioned particular integrations such as Performance Max that helps advertisers find incremental conversion opportunities and progressing rapidly.

One other curious thing that called my attention was the amount of time dedicated to YouTube. Management is really seeing a path forward with the platform and explained their thesis goes around 4 points:

“And to support this growth, we’re focused on, number one, Shorts; number two, engagement on CTV; number three, investing in our subscription offerings; and 6 number four, a longer-term effort to make YouTube more shoppable.”

The second wide matter of concern was cost discipline. Alphabet is focusing on making their cost structure as efficient as possible and said they have ‘significant multi-year efforts underway to create savings’. Among them, improving machine utilization and reducing the cost of scaling ML models, making data centers more efficient and better managing their real estate portfolio. Even though headcount grew 16% YoY, it barely did so on a sequential basis and management said the following:

“with respect to headcount growth, the reported number of employees at the end of the first quarter includes almost all of the employees impacted by the workforce reduction we announced in January. We expect most of the impacted individuals will no longer be reflected in our headcount by the end of the second quarter.”

My take

I think Google’s quarter was decent. We saw improvement in profitability and rebounds in many growth areas. I did expect management to be more aggressive with regards to their cost discipline, I’ll be very attentive to see them really tackle down that point. Finally, all business units experience a truly abnormal growth during the pandemic, for which, as I said, digestion is necessary and natural. Nevertheless, I’ll be paying close attention to see a more serious return to growth as quarters go by. I believe Alphabet should have no problem in returning to such road.

Personal commentary

I’ll be covering Texas Instruments and Visa’s earnings as well. You can subscribe below to receive them at your email!

Disclosure: This is NOT financial advice.

Any comments on SBC use and impact on FCF?