Google’s parent company, Alphabet, reported its fourth quarter earnings results, which looks like a mixed bag, as it has been happening with most companies for the past quarters.

Total revenue grew 1% YoY, from 75bn to 76bn. If adjusted by currency impact, they grew 7%. Gross profit was 40.7bn for the quarter, with its margin being 53%, down 300bps. In the same line, operating income decreased year over year, from 21.8bn to 18.1bn, causing its margin to drop by 500bps. Lastly, Google made 13.6 billion in net income, down from the 20.6bn earned in the comparable quarter from 2021. Net profit margin was down 900bps YoY to 18%.

Lastly, from one more operative perspective, Google did 16bn in free cash flow, down from 18.6bn in last year’s quarter, but flat QoQ. Free cash flow margin was at 21%, which was down 380bps YoY and 200bps sequentally.

All these are fundamentally bad. Declining financials are not sign of a healthy business, or at least a healthy period. However, it has been this way the past quarters for Google so it is not a big surprise. In this 4th quarter, margins dropped by the following bps YoY:

Gross margin by 270bps

Operating margin by 700bps

FCF margin by 400bps

Net margin by 800bps

2022 has been a year in which the company apparently lost some of the efficiency for which it was known, which is attributable to two things. Firstly, always when comparing financials year over year or whatever, make sure the base period is not an outlier. If it is, it will of course kind of bias the current results, turning the comparison into at an least innacurate one. The following chart gives some perspective on Google’s margin oscillation.

In the fourth quarter of 2021 Google had:

Gross margin of 56.2%, actually lower than the 10yr average, making this Q decline look worse. 2013-21 average GPM was 58.1%

Operating margin of 29.1%, 500bps above the 10yr average of 24.17%

Net profit margin of 27.4%, 600bps above the 10yr average of 21.5%

Yes, 2021 was an outlier, which makes a comparison to it kind of weaker than first perceived. The explanation to why did 2021 see such an upside in margins is partly due to the following, mentioned by management on the 3rd quarter’s earnings call.

“some of the margin upside last year was due to timing issues. And we had a very strong growth in revenues, a surge in revenues and a lag in investments that we said was a timing difference. And you are seeing some of that here.”

The mistiming of investments and growth can be seen in some operating expenses like R&D and CapEx. Good sign though that S&M went down YoY.

If we compare Google’s reported margins versus the 10 year averages, they didn’t look extremely bad. GPM was down 510bps against the average, operating margin was only down 40bps and net profit margin was down 350bps.

The second point I want to raise is headcount. We’ve seen an overhiring spree in big techs in all 2020-21, now their operating margins are paying for that. Google’s number of employees increased 21% in the past year and 2% since the last quarter, which resulted in an unbelievably high expense. Even more, given Google’s revenue only increased 1% YoY. These 34k extra employees imply Google is paying an extra 5.1bn-10.2bn dollars, under the assumption of an average salary of 150k-300k.

This concern has already been addressed by all big techs, including Google, which announced 12k layoffs two weeks ago. That’s a 6% of its workforce, not even close to the increase headcount has seen over the last years, but it’s at least a sign management is working towards efficiency.

Segment Analysis

Here’s what the company reported in their press release.

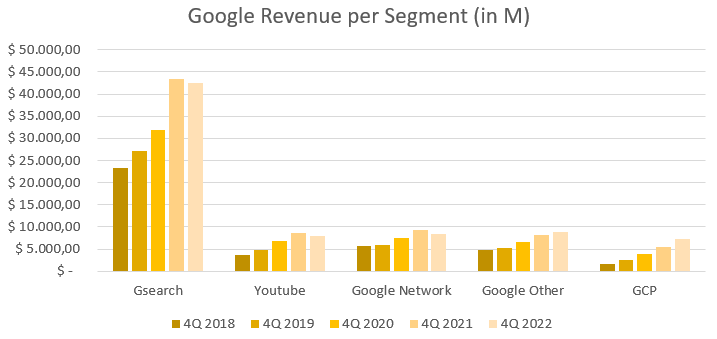

Again, we have to revisit Google’s past to see if the comparison is being made against an outlier. For it, I did the following chart illustrating each segment’s reported revenue as last years’ 4th quarters went by.

The most noticeable observation to be made is the abrupt jump Google Search saw in revenue over 2021’s fourth quarter. In 2019 and 2020 it grew at 16% and 17%, while in 2021 it grew at a 35% rate. If a company experiences such abnormal growth in a given quarter, deceleration in the subsequent quarter is to be expected, while the business ‘digests’ this outlier. That’s called a ‘tough comp’ to compete with, which is why Google Search revenue decline do not alarm me at all and even more so given its size.

The following table shows last fourth quarters growth per segment.

Even though the sated above is true for Google Search, I find YouTube’s decline quite concerning (I’ll further address this on ‘My Take’"). YouTube is a 32bn run rate business unit, which is large, but nowhere near close GSearch and it last year’s quarter was not an actual outlier. Furthermore, almost all YT ‘peers’ outperformed YouTube this Q. For instance, LinkedIn’s ad segment grew by 10% and Amazon’s by 19%. On the other hand, Meta’s revenue was kind of in line with YouTube and GSearch, declining 4% YoY.

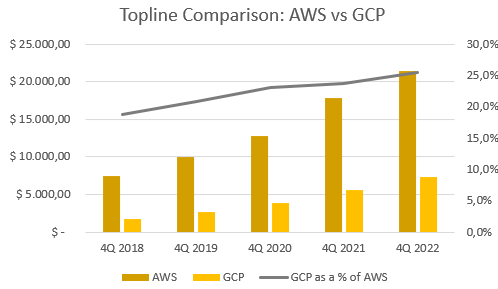

The last segment I’m looking at closely is Google Cloud Platform. GCP’s revenue grew by 32% this Q, decelerating from last year’s 45% and from last quarter’s 38%. This segment has grown to a considerable size, now being an almost 30bn run rate company. Growth is always expected to go down as businesses grow, it is only natural, so not that concerning. What I’d emphasize is its continued outperformance. Azure this quarter grew its topline by 31% and Amazon Web Services by 20%, making Google’s performance better than what could have been. Of course, its peers are much larger so it’s also natural for them to slow down, but still, it's worth mentioning.

One other thing I wanted to state was the decrease in Traffic Acquisition Cost, which declined 3.7% year over year, maybe partly explaining this overall decrease in GServices’ revenue.

Operating Income by Segment

Past topline and moving to the operating income each segment has produced over the last quarter, we get to the following.

As above, we’ll break down the operating income each segment has had and plot it along the last years’ performance.

Google Services have accounted for all operating income the company has basically ever produced, since other bets have been in negative territory for a while and GCP is a relatively new business unit (wasn’t even reported in 2017/18). Same pattern as with revenue repeats itself.

The table above showcases how much did operating income grew or decreased. It is again noticed the very rapid rise in GServices operating income though, on this occasion, it happened three years in a row. Google Services grew its operating income by 202% over 2017-2021 while its revenue grew 88%. Such operating leverage is extremely positive for the company, but the abrupt rise makes me stand in the same line as before, a slow down oreven a retracement is only to be expected. Year over Year, Google Services revenue declined 3.5% and its operating income 19%, somehow filling the wide performance gap created.

Now, the most positive aspect Google earnings have had, Google Cloud Platform’s operating performance. GCP has been growing absurdly fast, multiplying its size by 4 times in the last 5 years. However, this is not growth at all costs, the business unit has been rapidly improving its profitability, with its operating income almost turning breakeven. What’s particularly spectacular is how this player has been able to push its way into eating some of the older and more established players while still improving fundamentally.

I’d like to include Azure in the equation, but Microsoft does not report Azure’s actual revenue, but it includes it in the overall IC segment and/or in the Cloud Business.

Management Commentary

“First, the AI opportunity ahead. AI is the most profound technology we are working on today.” (..) “We published extensively about LaMDA and PaLM, the industry's largest, most sophisticated model plus extensive work at DeepMind”

They mention it’s not long until their AI work gets more broadly released through APIs, tools and add-ons to existing products, benefiting multiple disciplines as well. They mention that businesses, leveraging a Search AI feature, are seeing an average of 35% more conversion.

KEY NEWS: “To reflect the increasing DeepMind collaboration with Google Services, Google Cloud, and Other Bets, beginning in the first quarter, DeepMind will no longer be reported in Other Bets and will be reported as part of Alphabet's corporate costs.”

“We are committed to investing responsibly with great discipline and defining areas where we can operate more cost effectively”

YouTube Shorts revenue sharing just began. YTS is at 50bn daily view, up from 30bn in Q1

YouTube subscribers surpassed 80M. This happened in November and was up 60% YoY

“In 2022, more people created content on YouTube than ever before, long-form, short-form, audio, podcast, music, live streams,”

Market share was gained across hardware markets (mainly Pixel phone)

“Our machine learning infrastructure with cloud TPU v4 Pods can run large-scale training workloads up to 80% faster than alternatives according to third-party benchmarks”

“We are on a multiyear mission to make Google a core part of shopping journeys for consumers and a valuable place for merchants to connect with users” (..) They saw an uptick in merchants and inventory going to Google.

59bn worth of stock has been repurchased in 2022

Google Workspace's got to increase paid seats and revenue per seat

My Take

When I began looking at the results, I was actually quite disappointed as I have been with almost all Google’s 2022 earnings results. However, while going in a detailed way through them, I think Google has performed decently. It is all about perspective. A year over year comparison makes these results look extremely weak, though a bit of zoom out and context provides us with a somewhat different image.

This is by no means a justification for a bad performance overall throughout the past year. I do not believe Google did well in 2022, more so given how recklessly has management handled their cost situation. At the same time, Other Bets on Google have been showing VERY poor results almost forever, with 2022 having contributed 1.1bn in revenue while having an operating loss of 6.1bn.

Two weeks ago, they recognized their mistake and started working towards efficiency, as most big caps have, which, in some way shred some light to my biggest concern. On Other Bets, they said they would focus on better performing products and an overall goal of working towards profitability and efficiency.

Google Search performance was completely in line with my expectations this past year. Given the impressive growth it had in 2021, it was only reasonable to think a retracement or a slow down was due. In 2021, Google Search grew at 43%. With this last quarter results, we now have this business unit growth in 2022, which was 9%. Growing 9% over 43% at such scale is a respectable achievement in my opinion, considering how the macro has impacted all businesses through FX headwinds and how particularly weak has the ad sector been.

On GCP, I believe I stated my view, but anyhow, I think Google Cloud Platform is performing very well.

YouTube’s advertising topline is the most concerning factor this report has had. However, the ad sector has been very weak this year and YouTube’s ad business is suffering from in-house headwinds:

Subscriptions are not reported in the ad business

YouTube Shorts are still not properly monetized, taking share from YouTube long-form videos while not adding to revenue

If subscriptions were taken into consideration when seeing YouTube as a whole, topline would have probably grown (can’t estimate how much). 2023 will be more focused on monetizing Shorts, so I believe it should start being a tailwind moving forward.

Personal Commentary

I’m getting short of words on each article I write, but I do not want to overwhelm with information. I hope you enjoyed this review as much as I had writing it! If you have, feel free to subscribe below, I’ll be covering some more companies this earnings season. Lastly, I have a Deep Dive on Visa coming next week.

Disclaimer: Not financial advice.