Perhaps you noticed. I’ve been lately struggling in some sense with this notion that returns (not only financially) rely only in the future. However, its extreme unpredictability puts us in the position of attempting to try design and follow the best course of action without knowing if it will work or not.

This not a novel nor brilliant idea, it’s simply life. Nevertheless, encountering these ‘obvious’ concepts in the form of articulated writing can sometimes be eye-opening. Investors deal with the future in many ways and mechanisms, one of them being DCF models. I suppose most of you are familiar with discounted cash flow models, but, in case you are not, I’ll take the time to go through them, as we’ve done with several things.

I always try to understand why things exists, from a fundamental perspective, what problem does it solve and what it’s for. The price of an asset will be equal to the cash flows such asset will produce, discounted to today’s value. Having this idea in mind, one could aim to calculate the intrinsic value of these assets by forecasting the cash flows it will produce. Discounted cash flow models do exactly this and the ‘intrinsic value’ can be compared to the asset’s market price to determine if it’s correctly priced or not.

How are they done?

The formula is quite straightforward:

What you basically do is adjust the value of the future cash flows by the time variable. The further in time a cash flow is, the less it will be worth today. We could construct the formula upon three different steps:

Forecasting the cash flows

Calculating the appropriate discount rate

Calculate the terminal value

Investors generally utilize the free cash flow as the metric to forecast and the forecast is completely personal. One should think what the future growth of a company could be and the margins it could have. Of course, this is an overly simplistic manner of describing the task at hand, since investors should theoretically take every single variable into consideration.

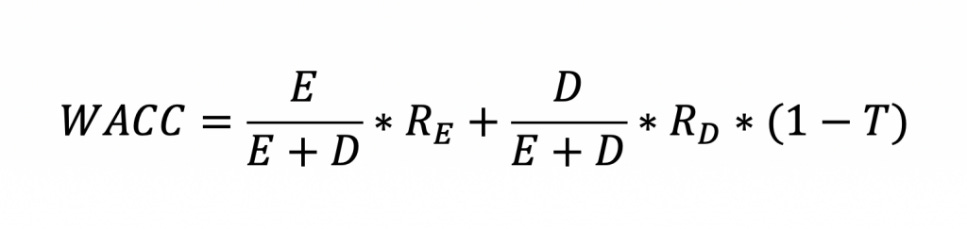

As per the discount rate, the commonly followed approach is to utilize the weighted average cost of capital (WACC).

The WACC, as the name implies, represents the company’s cost of capital from all sources, taking their weight into account. It’s thought of as the most appropriate discount rate because it is very comprehensive and unique to every single firm. The latter is of extreme importance because not all companies have the same difficulty when accessing capital and not all projects have the same risk.

The last part of the DCF equation suggests that one would need to forecast every single cash flow the business will produce for its remaining future. However, given the impracticability of the matter and the implausibility of doing it correctly, the financial community has opted to skip this part and, upon year X, replace the remaining future with the company’s “terminal value”.

The objective is to put in numbers this perpetuity of cash flows a company ‘will’ have. After a certain period of time (generally 5-10 years), investors decide to ‘summarize’ the remaining cash flows into this equation. They assume the business will produce X cash flow in that year and that it will grow at a g rate for perpetuity.

Short Thoughts

Figuring out ways to handle the future is no joke. I think DCF models are a good way of dealing with this phenomenon. This thought would perfectly fit into the narrative Terry shared in one of his letters (which I covered):

“The commanding general is well aware that forecasts are no good. However, he needs them for planning purposes.”

Additionally, it forces one to actually draw what they expect the future of a company will look like. Perhaps by doing so, the growth rate and the expenses we think the business could have might get clearer. Otherwise, our own expectancy of the company’s future could remain somehow uncovered. Knowing what we think is much more complicated than it seems and these kinds of practices sometimes help dismantle thoughts and ideas.

Huge however, the chances of having an accurate model are 0 and the sensibility numbers have is ludicrous. If we were to change one single percentage point in the discount rate, the ‘intrinsic value’ we would obtain would be absurdly different. How could one make investment decisions based on such a flawed mechanism?

Personal Commentary

I tried to keep thoughts as short as possible, though I’m sure I left many out of this article. I’ll be revisiting this particular topic in the future, when I think I’m capable of adding some value on the philosophical front. Hope you enjoyed the write up!