In continuation of ‘Income Statements’, published three weeks ago, we’ll be covering today another major component of the Financial Statements.

Cash Flow

Firstly, as the name indicates, this sort of Statement is about Cash Flow. Cash Flow refers to the net amount of cash & equivalents that comes in or goes out of a company in a determined period. Logically, it tracks the flow of cash. Receiving cash is called an inflow, while spending cash is called an outflow. There are multiple streams from which a company could be receiving cash or spending it. The cash flow statement allows you to identify these and assess management’s use of what actually matters to every business, money.

It is financially considered that money can be received from or spent in three different categories, each of them representing a part of the cash flow statement. Before going into the three segments, note that as we are calculating a change of cash, a positive number would imply an inflow and a negative, an outflow. I say this because it gets tricky. For example, depreciation is a theoretical cost, though a company does not have to use actual money to pay for depreciation of its equipment, therefore it represents an inflow of cash.

Cash From Operations

Operations alludes to business related activities, from the chain of production to the sale of goods and services. Cash From Operations implicates the amount of net cash received or spent in ordinary operations. Therefore, the capacity for a business to generate a positive or inflow of cash in this regard would imply for the company’s ongoing business to be naturally profitable. It indicates whether a company can generate enough cash flow to maintain and expand its current operations or, otherwise, if the company can’t maintain its operations through the profits made by them.

This segment is done by reconstructing from the bottom of the Income Statement upwards. From net income, which would be the absolute inflow or outflow of money, to each item that added or subtracted cash to this final number.

All subtitles seem very transparent so I won’t go through them individually. The only one kind of tricky in here is ‘Stock-based Compensation’, which is an operating expense (remember income statements), and would be for the company to pay employees in its own stock and not purely in cash. That’s why it’s a positive item in the cash flow statement. Beware of this expense since the higher it is, the higher the dilution shareholders suffer (shares in circulation would go up so each individual share should be worth less).

Cash From Investing

The name is very straightforward. Cash flows from investing reports how much cash has been generated or spent from various investment-related activities in a certain period. It can include purchases of securities, sale of securities, purchases of speculative assets and there’s one particular one on which I want to make emphasis.

In this section is where Capital Expenditure makes its appearance. CapEx is money invested by a company to acquire, upgrade or maintain fixed, physical, non-consumable assets, such as buildings & computers. There are occasions in which the business could be making an investment in a new building or improving one to increase production capacity. However, in not few occasions, companies need to recurringly make ‘investments’ in current property & equipment to maintain them.

Upon Cash From Operations and CapEx, a widely used concept arises, Free Cash Flow, (CFO – CapEx). Free cash flow is the ultimate representation of a company’s business actual profitability. The reason being that it’s the money made through operations and after investments to enhance and maintain such operations are done.

Cash From Financing

Shows the net flows of cash that are used to fund the company and its capital. Financing activities include transactions involving issuing debt, equity, paying dividends, repurchasing stock. Cash flow from financing activities provide investors with insight into how the capital structure is managed.

After all these three methods that originate an inflow or outflow of money, we get to the final part. The net change in cash is simply how much money did the company start the period with and how much did it have left at the end of it.

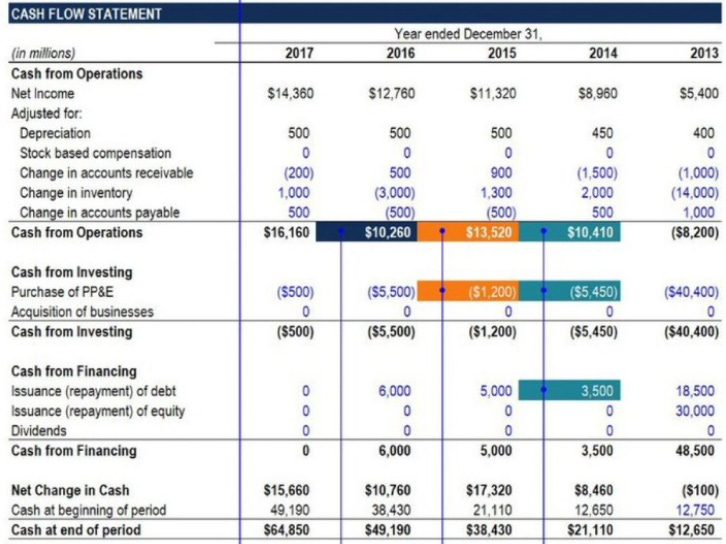

For you to get a more real glance at what Cash Flow Statements look like, here is the one Google presented at its last earnings results. If you watch closely, not only is the structure the same as the previous one, but most item titles’ are very transparent, which facilitates comprehension.

Conclusion

Cash flow statements are a very powerful resource investors get from public companies. From them, you can infer how well does the business manage the money it flows through it, and that’s no joke. Investing in the stock market is about appreciating your own capital and analyzing things like this can help you avoid mismanaged companies and walk a step closer towards well managed ones.

Personal Commentary

I know financials make absolutely no sense at first. One has to be exposed to a lot of them to start internalizing concepts, though I hope to have accelerated your learning curve at least a bit, for compounding to begin earlier.

Excellent post G. Cash flow statements are so important. I emphasize OCF and FCF.