Investors speak about business models all the time, but there’s rarely someone who stops and defines what a business model is. Definitions are never easy but, without a definition, the most likely thing is that everyone will be talking about different things. Fortunately for us, Clayton Christensen defined the fundamentals of what makes up for a business model. In this article, we’ll go over these and add a bit of depth, leveraging Mauboussin’s research articles.

Business models

‘A business model, from our point of view, consists of four interlocking elements that, taken together, create and deliver value’. These four elements are:

Customer value proposition. When a company finds a ‘job needed to be done’, it has successfully found an objective that would allow it to create value. After the job is identified, it is about thinking about what the offerings should be and how would they be distributed. The better the business does the job, the greater the customer value proposition.

Profit formula. This consists of how will the company capture value from the value it creates. The things to consider are the revenue model, the cost structure, the margin model, and the resource velocity. With scalability and the key costs in mind, there’s always some sort of margins and asset turnover the company has to aim to in order to create value profitably.

Key resources. Key resources include ‘the people, technology, products, facilities, equipment, channels, and brand required to deliver the value proposition’. Clayton underscores the importance of identifying the crucial elements that create value and how they interact with one another.

Key processes. At the core of companies, there’s always people. To make the business deliver the value in a repeatable and scalable manner, there are operational and managerial processes that have to be in place. Things such as training, development, planning, manufacturing, sales, rules and norms, are part of the key processes.

Business models, then, depend on how companies arrange and interlock these components. Even though there are infinite permutations, Clayton’s team identified three fundamental business models, which compose what would be the very basis for all of them.

Solution shops. These are companies that solve complex and unstructured problems for customers. Solution shops diagnose the problem and propose a solution. They charge a fee for service.

Value-adding process. Things come to these places, value is added to them, and they go out. VAPs fix broken things and include things like manufacturing, which brings together multiple otherwise isolated components. Value-adding processes are generally charged for the output.

Facilitated network. Some businesses own a network that allows customers to trade (whatever product or services) between one another. The network-owner charges fees per transaction.

Now that we have laid the foundation of what business models are, there’s room for diving into Mauboussin’s subject-specific insights. I kept reading Michael’s research articles, and I’m now at article number 18. Turned out being a very insightful and, curiously, easier read than expected.

Cash economics of business models

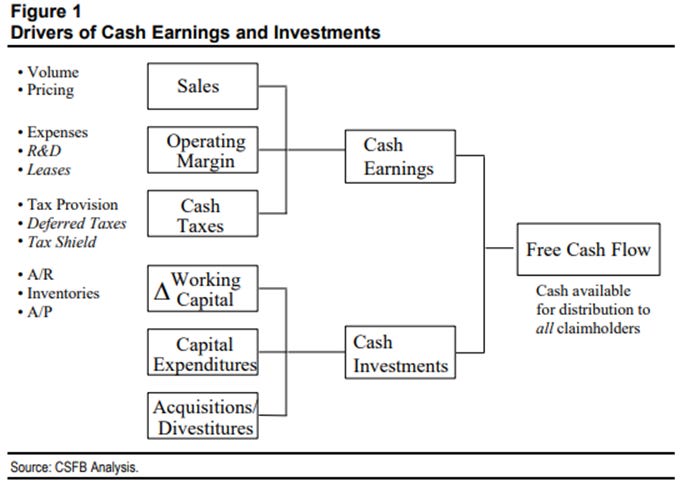

A business is worth the future free cash flows it will produce discounted to today’s values. Logically, when trying to value a company, one has to think what these future free cash flows would look like, considering its two components:

Cash earnings is the operating income the business produces minus its cash taxes

Cash investments include changes in net working capital, investments in fixed assets and M&A

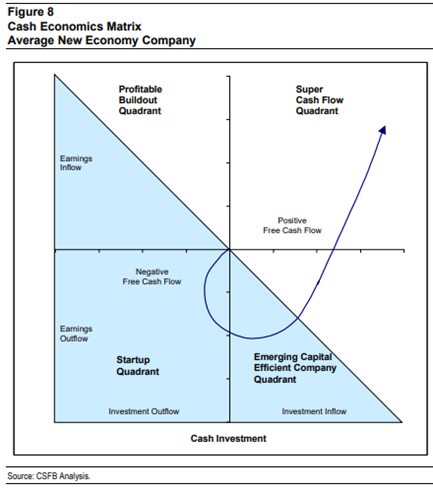

The interesting thing though is that, depending on how the company generates or consumes cash, the business model it has. According to Mauboussin, there are four fundamental ones:

Profitable build-out. Encompasses, mostly, traditional companies, which have cash inflows from earnings and outflow from investments.

Startups and value-destroyers. These companies have outflows from earnings and from investments.

Turnarounds and emerging capital efficient companies. Outflow from earnings and inflow from investments; generally temporary.

Super cash flow. Inflow both from earnings and investments. “Only a company with a cash-efficient business model — its customers pay it before it has to pay its suppliers — can stay in this quadrant for long”.

Cash economics lifecycle in the old vs new economy

Michael, after understanding how cash economics work on both types of businesses, seems to have spotted a recurrent pattern. I’m still digesting this, but it is like if companies, depending on their essence, will have a certain trajectory of cash economics. What’s curious here is that, if we are able to categorize companies by essence, the most likely thing is that they follow the baseline for this cash economics lifecycle. That is, if it doesn’t go bankrupt in the process.

For example, the average (among successful) old economy company seems to begin, as all, at the startup/value-destroyer quadrant, and moves up into the top-right of the profitable build-out quadrant. However, its essence does not allow it to escape from that quadrant, as it needs investments to keep growing. The company’s annual investments tend towards its “economic depreciation, resulting in a net investment of approximately zero and a stable cash earnings base”.

On the other hand, successful new economy companies have a very different cash economics lifecycle. They begin as a startup, move into the emerging capital efficient quadrant and, as they get scale, move into the northeast of the super cash flow quadrant. The reason they get to the latter, I suppose, is that these companies can charge from customers before paying its suppliers, leading to actual income from investments, and they have close to 0 new investments in fixed assets.

Personal commentary

It’s fascinating to start analyzing fundamental principles from different perspectives. There is a lot of value to bring from Mauboussin’s research and multiple connections to make with theories we covered. Hope you enjoyed it and will try for the next one to be in this line as well!

Contact: giulianomana@0to1stockmarket.com

Today’s podcast episode: From 0 to 1 in the Stock Market, Podcast

Thanks my friend!