Burford operates in the legal finance industry. It offers exposure to a sector that’s incredibly profitable and one which does not offer many options in the public markets.

The company has achieved a 27% IRR with its capital provision since inception in 2009. Management deployed 1.3bn dollars and has realized over 2.48bn, considering concluded cases. Curiously, this is achieved by investing in assets that are uncorrelated with one another.

Although Burford has led the industry, competition is catching up. Capital in the industry is perceived as a commodity and people fear that excess returns will vanish. In this article, I’ll dive into what is Burford’s strategy to eschew competition.

Industry Context

Legal finance is an industry of capital deployment and reinvestment of the proceeds. Having emerged 20-25 years ago, players are still gaining scale, which can be accelerated by raising and managing private funds. As an indirect consequence of the industry’s recency, Burford is one of the only large public players.

Management stated that information concerning competitors is mostly limited. Most of them do not disclose returns publicly and, in multiple cases, not even assets under management. Nonetheless, the company was not the first mover in this space and has faced continuous competition since inception.

Although industry returns are very appealing to firms and hedge funds, given IRRs and uncorrelation between assets, there’s a caveat. It is not possible to predict with a high degree of confidence how cases will evolve nor how much time it will take for them to be resolved. Burford’s management claimed that, otherwise, you wouldn’t see these returns and competition would’ve more rapidly flooded the space.

In fact, being Burford the leader and “only” having 7.1bn in assets under management only confirms the hypothesis. I suspect firms’ AUM would be substantially larger if returns were of a higher likelihood. Private equity might act as a valid comparison in this regard. Although its inception can be traced back to the 1950s, proper activity emerged in the 1960s and further strengthened in the 70s. Private equity’s high returns, which might be perceived as highly attainable, has gathered trillions of capital in a couple of decades.

Legal finance addressable market is smaller, but it has been the case that raising capital has been comparatively slower. It’s estimated that assets under management for the industry in the US is at 13.5bn.

The last time Burford shared AUM data alongside its competitors contained end-of-2022 numbers. At the time, it had assets under management of 5bn (ex BOF-C). In contrast, its nearest competitor had raised a total of 1.9bn dollars, which, although not disclosed, I suspect corresponds to Omni Bridgeway. The latter has been transitioning from a balance sheet investment approach towards pure asset management. This implies its income will depend solely on fees, whereas Burford will benefit from the returns of its 4bn+ balance sheet investments.

As of February 2024, Omni Bridgeway has 2.5bn in funds under management.

The more capital a company raises, the larger its addressable market. Legal finance, as exposed, offers a broad range of assets to invest in, varying in expected risk, return, duration, and nature. At the foundation of everything, however, there’s litigation finance. Funding a single claim’s legal fees might require as little as 100 thousand dollars to 15M. However, as legal finance evolved, a trend made itself clear.

Aiming for the High-End of the Industry

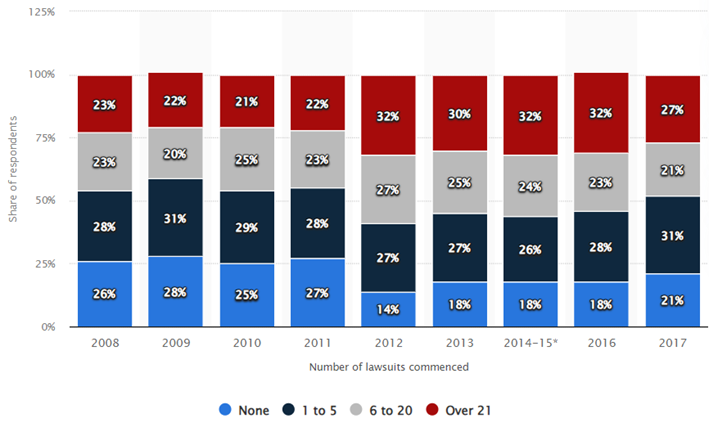

As companies’ operations expand, they start impacting more people, and as that occurs, damages are spread wider. Therefore, the bigger businesses get, the more lawsuits are filed against them. In fact, this article reveals that, as of 2005, around 90% of US companies were dealing with at least one litigation, with the average company juggling 37 lawsuits at once. Companies with over 1bn dollars in revenue faced an average of 147 lawsuits.

In 2015, BusinessWire reported that the litigation budget for US companies was rising. Noticeably, “Respondents also reported an increase in the percentage of US companies with litigation budgets of US$10 million or more (25% percent, compared with 17% in 2012). Another report, from Legal Dive states that companies with 5-20 billion in revenue saw their median spending in legal issues rise by 45% YoY to 30M in 2023.

Statista’s chart shows a survey that was done to different businesses. They were asked how many lawsuits were commenced to them in the past twelve months.

What this translates to is more spending by larger corporations. For them to find use in legal finance firms, the latter should have a certain scale and be able to rapidly deploy tens or hundreds of millions of dollars. At the same time, corporations need to partner with a well-respected and capable legal financier. They need to not only receive funding, but smart funding. In response, Burford has focused on developing a breadth of skills and solutions, so that they can efficiently address the verticals of needs clients may have.

“Clients come to Burford— and keep coming back to us—because we add value” 2021 Annual Report

From the legal finance firms’ perspective, it is virtually impossible to scale operations without going upmarket, unless the company takes a decentralized approach towards capital allocation. The smaller the average deal they make, the more of them will need to be done to increase profit in absolute terms. In Burford’s 2021 Investor Event, management said their commitments were averaging $21 million, up from a previous $8 million size.

Portfolio of Claims

At the beginning, 100% of Burford’s business revolved around funding single case litigation. Very rapidly, management found that it is inefficient for large corporations and law firms to seek capital for each litigation they are facing. In consequence, the “portfolio” approach arose. Law firms ask Burford to finance a group of claims, ultimately favorable for both parties. This way, Burford spreads the investment risk across uncorrelated assets, decreasing the chances of binary loss and allowing the firm to offer more favorable terms. Additionally, it allows Burford to deploy more capital.

In its 2022 annual report, the company disclosed that their biggest relationship with a single law firm accounted for $334M in commitments on a group-wide basis and $201M on a Burford-only basis. These equate to 8% and 7% of commitments, on both basis, respectively.

The relationship consisted of: “(i) financing arrangements between us and the law firm, where the law firm seeks to monetize the risk that the law firm has taken with some of its clients, (ii) direct financing arrangements with counterparties that elect to hire the law firm where our financing funds the law firm’s legal fees and (iii) direct financing arrangements with counterparties that have hired the law firm but where our financing is used for other corporate purposes than for funding the law firm’s fees”.

The Key Element for Scaling: Monetization of Claims

Initially, what would normally occur is that corporations wanted to pursue legal action, but they did not want to pay law firms an hourly fee. In these cases, it was in the law firms’ best interest to find a legal finance business to fill the gap. This caused Burford to first develop good relationships with legal companies. After some time working together, law firms would act as originators for Burford, which in many cases ended up in Burford funding a portfolio of litigation claims.

The problem that derives from this dynamic is that providing relief only for corporations P&Ls, by paying legal fees, imposes a natural ceiling for capital deployment. Burford could only scale its business up to what legal fees cost.

“it's not uncommon for us to be funding $7 million, $9 million, $10 million, $12 million for legal fees and expenses in a case. But once you get above those numbers, it does become relatively uncommon to find a case both that needs $20 million, $25 million, $30 million of legal fees spent on it. And so, you simply don't see cases that large.” 2021 Investor Event

Once Burford gained brand recognition, corporations started knocking on its door. Generally, the starter deal is the same as before, given it’s the most well-known service that legal finance offers. It provides funds for legal fees, improving corporations’ income statements. As the relationship between the two evolves, companies notice they can utilize Burford’s funding for other purposes, the most prominent of which is monetizing their claims.

In addition to providing corporations with the funds for legal fees, Burford offers an upfront payment in exchange for a share of the proceeds, plus a return on the funded cost. The upfront payment is seen as the expected value of the litigation claim discounted to today. This allows clients to “convert an intangible claim or award into tangible cash on a non-recourse basis”. Importantly, the market generally assigns no value nor relevance to such intangibles.

The monetization business has rapidly grown as corporations realized how beneficial it is from an operating perspective. In 2019’s conference calls, management pointed out that demand for monetization was trending upwards. In 2018, monetization and claim family commitments represented 34% of Burford’s group-wide capital provision. For capital provisions made in 2021, their share grew to 53%.

This is ultimately positive for Burford for three reasons: (i) it allows management to deploy more capital on cases where they desire more exposure; (ii) monetization of claims help increase overall deal size, because, for example, legal fees for fighting a case with a potential settlement of $50M to $500M are the same, but the room for monetization is gigantic; (iii) it helped Burford build relationships with corporations, which are now providing the fuel for a new growth stage.

On the first point, once Burford gets involved in a specific claim, the team gets to know everything about it. Burford can utilize its knowledge in the claim’s respective circumstances to help other companies pursue claims alike. This implies not only more exposure to a desired asset, but operating leverage as well. Due diligence is already done and no expenses on headcount are required. Additionally, new customers will be sure they are getting access to smart capital.

The company reported that corporations made up for 57% of total commitments by the end of 2022, up from 35% in 2016. In Burford 2021’s Investor Event, the company disclosed that “72% of clients who have done one deal with us come back for more”. The following chart displays most of the features discussed in the previous paragraphs.

In the third quarter of 2023, management mentioned the fact that, in any given period, the firm’s commitments will be driven by large corporate deals. In the second quarter, for instance, Burford committed 325M dollars to a Fortune 50 company. Likewise, in 2019, Burford committed over 140M to Sysco, for the latter to monetize a series of claims.

Access to capital, and being able to rapidly deploy it, provides Burford with a competitive advantage with respect to most of its peers. Having foreseen this, management entered the asset management business in 2016, when it acquired GKC. To scale relationships with corporations, Burford has to commit sums of capital in excess of 100M dollars. When management does not want complete exposure, it funds the client with Burford’s balance sheet and capital from the private funds it manages. Similarly, the combination allows Burford to make deals they couldn’t afford on their own.

The Advantages of Scale: Data, Branding and Flywheels

In litigations, most information only becomes public when the trial verdict is reached. However, the latter occurs in less than 3% of civil cases, according to this Article, while Burford estimates that “about 90% of disputes settle”. When parties settle, the most likely thing is for the mutual agreement to include a confidentiality clause. Consequently, most case-related information remains private, only known to the parties involved. Outsiders can’t even tell the dollar amount for which parties settled. It therefore becomes difficult to build a large pool of actionable data. Burford has known this since day one and has focused on gathering this information.

Prior to underwriting, Burford leverages probabilistic modeling based on first party as well as third party data. Being the leader of legal finance since inception provides Burford with a unique advantage in this regard. It is the business that has historically funded the largest number of litigations. There is no other pool of data that closely matches that of Burford.

Additionally, this means that the bigger the scale the company operates at, the more exposed it is to different litigation matters. And because of the recurrence with which information remains private, Burford possesses and keeps strengthening its unique advantage with respect to smaller scale competitors.

Scale allows for funding portfolio of claims, which further enhances this. In the company’s 2015 annual report, it’s mentioned that “while Burford has 54 “investments”, there are now more than 500 separate claims underlying the investment portfolio".

Likewise, the larger the scale Burford acquires, the bigger deals it will do and with increasingly more reputable firms. Burford’s brand immensely benefits as a consequence. This turns Burford into the face of the legal finance industry. And, naturally, larger corporations will want to engage in deals with the most respected firm in the space.

“We believe that we are more visible than our competitive set in legal and business publications. For example, according to “share of voice” calculations using Muck Rack, a provider of public relations tracking software, we were featured in over half of the total articles about the legal finance industry that mention any pure play legal finance provider during the year ended December 31, 2022.”2022 Annual Report

Personal Commentary

Last Sunday, I communicated my intention of splitting articles and publishing shorter one, but on a more frequent basis. Any feedback on whether or not this is helpful is appreciated. Next article will be on the room that Burford has left for competition, and the industry fundamentals.