Burford Capital reported results for the fourth quarter of 2023 on March 14th. In this article, I’ll go over everything relevant for analyzing their yearly performance. This shall include portfolio-related information, management’s commentary, my take on the quarter and pertinent thoughts on Burford’s weight in the portfolio I manage. Furthermore, a shift in capital sourcing was made note of in the shareholder letter, on which I will expand accordingly.

The company finished 2023 with a group-wide portfolio worth 7.17bn dollars, representing an increase of 16% YoY. On a Burford-only basis, the portfolio ended at 4.84bn, up 22% yearly. It is important to note that the carrying value of YPF-related assets finalized at 1.37bn, increasing over 500M. The latter was caused by a decrease in these assets’ adjusted risk premium, falling from 38.1% to 30.2% at Dec 2023.

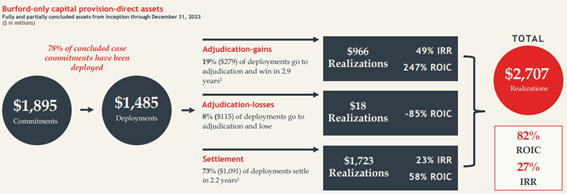

Last year’s performance put deployments and realizations at 1.48bn and 2.7bn, respectively. Since inception, Burford has invested its capital at an 82% ROIC and 27% IRR. The former of both experienced a decline of 500bps, mostly caused by a big investment that resolved in a quick fashion in the second half of the year.

During 2023, Burford committed 897M for capital provision-direct assets, slightly above 2022. Burford-only commitments were 691M, slightly down yearly. The company finalized 2023 with 1.408bn in undrawn commitments on a Burford-only basis, with 99% of the total being for core legal finance.

Total deployments, on a group-wide and capital provision-direct basis, were 530M, experiencing a yearly decline. Burford-only deployments amounted to 382M, down 17% yearly. Part of the slowdown was attributed by the team having to work on ongoing cases and for the rapid resolution of a big case.

Realizations were the highest Burford reported since inception, being 496M for the whole year and representing an increase of 41% YoY. Cash generated during 2023 was $415M on a Burford-only basis. Management mentioned throughout the quarters that the portfolio was acquiring velocity as courts worked through their backlog.

Although income and cash proceeds increased dramatically, so did operating expenses. Nonetheless, it is to be observed, compensations and benefits, mostly tied to investment performance, compose the vast majority of the increase. Long-term incentives accounted for over 110M in operating expenses, with 69M due to YPF’s increase in fair value. These bonuses are only paid after Burford receives the cash proceeds. The company ended the period with 162M payable for long-term incentive compensation, up from 61.7M.

“In the salary and benefit line, we were impacted by approximately $6 million to $7 million in the year, driven by the increase in our stock price (..) our employees have the ability to invest their deferred compensation in our stock and when the share price increases, we have an accrual expense. We look to offset that economically by purchasing shares to hedge that exposure.”

Capital Structure

In 2008, Chris started noticing the excess demand there was for funding litigation claims and thought he should take his hobby seriously. Alongside Jonathan Molot, both decided to raise institutional capital to address this unmet need. Burford’s IPO effectively granted the business with 130M dollars, which was rapidly committed and deployed. In fact, demand was so strong that Chris and John did a follow up in 2010. More equity was sold on a secondary offering for an aggregate of 175M dollars. Ever since, no more capital has been raised via this avenue. Rather, the team waited for their investments to yield results for writing more business.

In 2014, Burford started issuing debt in the UK market, though capital raises were barely moderate. Two years later, management acquired GKC, an investment management firm. The purpose of this acquisition was to invest in other verticals legal finance offers that they couldn’t do otherwise, for capital was a major constraint. Managing private funds offers flexibility and capacity for rapidly raising capital. Furthermore, some of these alternatives, like post-settlement, have decent expected returns with almost no risk, but considering management’s hurdle rate for balance sheet capital, they weren’t investing in these. This way, Burford grew its group-wide business to over 7bn dollars.

However, private funds’ commitments were taking share of the overall business. In 2019, out of 1.6 billion in commitments, only 726M were Burford-only. The former had quadrupled while the latter didn’t even double in the prior 3 years. Management mentions not to have liked this dynamic as shareholders themselves. Managing private funds ended up being a costly way to grow. Indirectly, it capped the company’s capacity to write new business and was poised to continue on such a path.

Notwithstanding this, I have some reasons to believe it had several positive side effects for shareholders. Private capital did allow Burford to make investments they couldn’t do otherwise. As mentioned, capital was a major constraint. Having passed the phase and counting Burford with more resources now, it would’ve been a mistake to keep running the business in this manner.

In consequence, management focused on accessing the US market. In 2020, they registered with the SEC and added Bur’s listing to the NYSE. This allowed the company to tap into the US debt market. Thereafter, Burford issued debt on four separate occasions.

This ought not to be overlooked, for it dramatically changes Burford’s economics:

“This cost of capital is game-changing for us. With 2/20 fund capital, we pay around 80% of investment profits to our fund investors for the use of their capital. Now, given the average 7% interest rate on our debt and the average 2.5-year duration of our matters, we are instead paying only a total of around 20% of investment profits for the debt, fundamentally changing the economics for the balance sheet.”

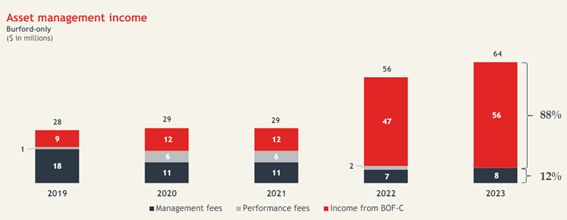

The team has hence been focusing on getting capital from this cheaper source and reducing their reliance on private funds. Their 2/20 structure turned out to be highly disadvantageous, considering the team’s skill. In fact, as the following image will illustrate, BOF-C is generating 88% of asset management income, although the portfolio is smaller than that of the others. It is to be observed that BOF-C fee structure differs from the rest of partnerships.

Burford closed the Strategic Value Fund and decided not to immediately replace Burford Opportunity Fund. New complex strategies investments will be carried out with capital from the balance sheet, if sound investments are found. Regarding their arrangement with a sovereign wealth fund, carried out through BOF-C, the agreement was renewed last year. Finally, another Advantage Fund will not be immediately raised after expiry. To the extent lower-risk legal finance investments are made, they’ll be done so with balance sheet capital.

Management Commentary

Christopher and Jonathan were mostly pleased with Burford’s results. Growth had been staggering since inception and, once they were preparing for the next stage, Covid hit. The closure of courts abruptly stopped momentum and hurt short term performance. In the meantime, management were seeing how much traction legal finance was getting and where they could go. This dynamic caused performance to be poor and management to sound as storytellers.

The velocity the portfolio acquired was notorious in 2023, as courts worked through their backlog. Multiple milestones were reached. Realizations, the vast majority of which were cash receipts, increased over 40% yearly. These elements are starting to back up management’s narrative. In addition to this, when combined with group-wide performance, they illustrate the team’s capacity to produce high returns at greater scale.

Christopher and John spoke about the nature of Burford’s business. Seasonality and large deals will impact quarterly numbers. A large part of commitments and realizations are done in the fourth quarter. And big cases, due to capital deployed since inception being 1.5bn, will have strong influence on exhibited ROICs and IRR.

Burford made a deal with a Fortune 50 in the second half of the year. The company committed $325 million and deployed $225M, with the remainder to be deployed in December. A rapid resolution didn’t allow for the last 100M in deployments to materialize. If the latter had occurred, Burford would have had record deployments, instead of a decline. Furthermore, the rapid resolution generated a 37% IRR, but a 36% ROIC. For the deal was big relative to Burford’s deployments, it naturally impacted both metrics, causing a 5pp decline in historical ROIC. Management stated not to be concerned with such a thing.

Finally, Chris talked about their cost structure. Analysts were concerned about the high increases in operating expenses. Management reminded investors that fixed costs are quite low. Most operating expenses are variable, which depend on the portfolio’s performance. It’s important to note that the vast majority of these are accrued expenses for future payment, “but we’re obviously not making those payments until we get cash in the door.”

My Take

I’m seeing the path forward quite clearly. I suspect this is not due to my deductive skills, but rather to management’s communication. In annual reports and shareholder letters, it made clear to me that these people say what they think about situations and how they will respond.

This shareholder letter, however, further clarified how they are thinking about capital sourcing. I believe the rationale behind the strategy is sound. For the team plans to maintain a debt-to-equity ratio of about 1/5, I find this incremental capital to be smartly raised and likely to enhance results.

Burford’s deal with the Fortune 50 company starts showing as well why the strategy was built around securing a spot at the high end of the market. There is no competition there. Although it may appear as if capital could create competition, I believe this hypothesis will be proven ultimately wrong, though it will naturally generate some pressure. Larger deals require higher degrees of value to be added.

This performance review allowed me to answer several questions I had. Burford’s weight in the portfolio is currently 2.2%. I intend to increase to 6.5% in the near future.

Personal Commentary

I decided to keep this review open for you to get a sense of how Burford’s coverage will look like moving forward. Hope you found it useful and I’d encourage you to subscribe to receive future ones.

Disclosure: This is not financial advice and should not be taken as such

Great review! After reading your deep dive and doing some research on my side, I'm starting to be pretty interested in Burford.