Earnings season is back. Before going into the article, reminder that I’ll be covering ASML, Tesla, Google, Microsoft, Visa, Texas Instruments, Zoetis and Mercado Libre in the next couple of weeks.

Overall Financial Analysis

ASML reported results on Wednesday’s morning. As usual, the earnings review will be split into three parts. We will first go over the business’ financials as a whole, taking pertinent detours, then dive into the revenue composition, and, finally, management’s commentary and outlook, followed by my personal take.

Note: keep in mind numbers are in Euros.

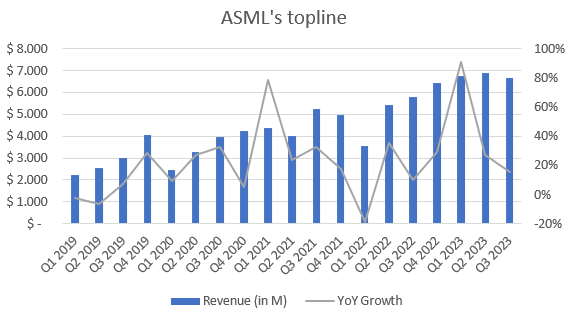

Revenue for the quarter came in at 6.67bn, growing 15.5% yearly and declining 3% sequentially. The compound annual growth rate for ASML’s topline sits at 19.2% for the past five years. Even though deceleration appears to be massive, the are two factors playing here:

This year’s first quarter saw abnormal growth not only for the strong report, but also for the extremely weak Q1 last year. If we remove the outlier, growth is in line with past quarters.

Over the last three years, photolithography demand exploded. After unusual spikes, which in most cases bring demand forward in some sense, digestion is needed.

There is some component of revenue that corresponds to 2022, which was delayed to this year due to a change in protocol.

“The value of fast shipments in 2022 leading to delayed revenue recognition into 2023 is around €3.1 billion” Q4 2022 press release

“As you know, we fast ship DUV immersion and EUV. But on DUV immersion we came to an agreement with customers, where we basically have a reduced test protocol. Which they now accept as good enough to basically recognize revenue when we ship the machine out of our factory in the Netherlands. Instead of taking revenue when we do the installation at the customer site.” Q2 2023

Having said this, and accounting for quarterly volatility, it has been remarkable how strong the demand for ASML’s systems is. While the semiconductor industry has been in a somewhat pronounced down cycle, the company has been able to sequentially grow for 7 quarters (until this one). In some line, such a feature reflects how crucial of an element are photolithography machines for semiconductor manufacturing, highly exceeding supply, and the value of having a large pile of bookings.

“our Public Chinese customers say: We are happy to take the machines that others don’t want” Q2 2023

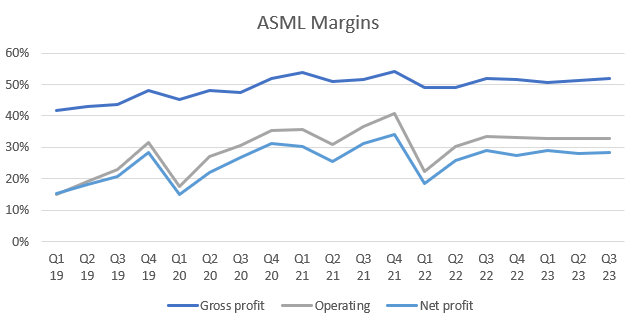

Moving down the income statement, the company reported 3.46bn in gross profit, implying a margin of 51.8%, which was flat year on year. Operating income was 2.18bn for this quarter, up from 1.93bn last year. The operating margin was 32.7%, down from 33.5% on the comparable Q. Finally, ASML generated 1.89bn in net income, meaning it operated at a 28.3% net profit margin, which experienced a slight compression YoY.

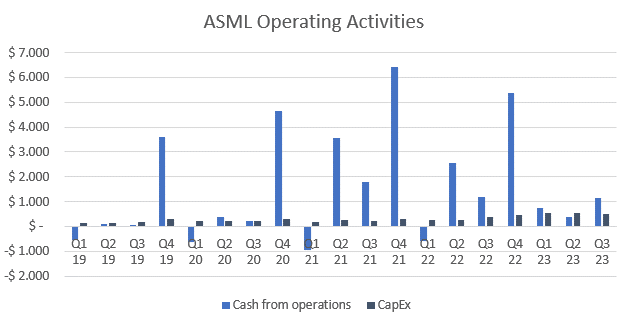

Turning our attention to the cash flow statement, ASML brought in 1.12bn in cash from operating activities, down 3.6% year on year. On the other hand, capital expenditure amounted to 501M this past quarter, very in line with Q1 and Q2, though an increase of almost 50% over the comparable quarter, affecting the resulting free cash flow. Given how much seasonality there is embedded in this business’ cash flow, quarterly numbers tell fairly little.

Revenue Breakdown

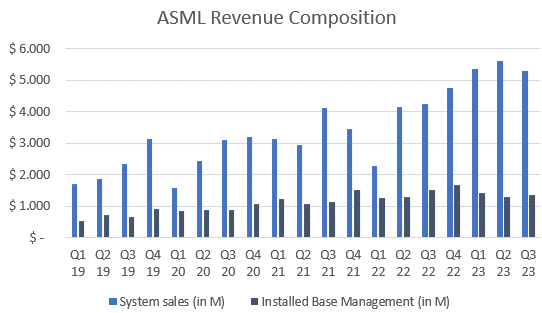

ASML derives revenue from two major sources. The first and main one consist in the selling of photolithography machines. On the other hand, installed base management encompasses support, upgrades and selling enhancements to further improve the performance of old systems sold.

In this last quarter, 80% of the company’s revenue came from selling lithography machines. As everything ASML-financial-related, the share of revenue is volatile. Although system sales appear to have been taking share of total revenue, at least since early 2019, their total share of revenue oscillates between 65-80%.

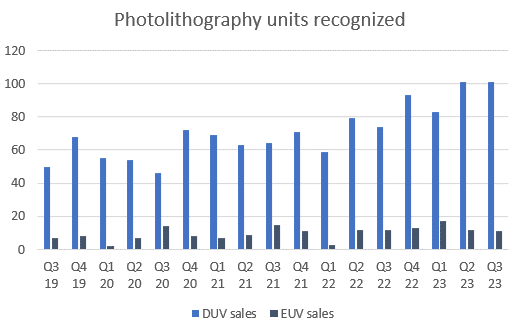

In addition to the aforementioned categorization, system sales revenue can also be split into two main products, deep ultraviolet (DUV), and extreme ultraviolet machines (EUV). During Q3, DUV sales were 101, while 11 EUVs were sold.

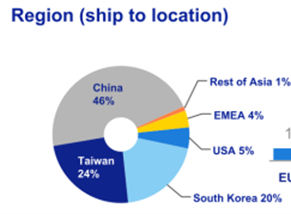

The company always discloses the region to which they ship their systems. This is a somewhat useful indicator to get a glance of the company’s geographical exposure. Out of the total, 46% of the systems were shipped to China, 24% to Taiwan, 20% to South Korea, with the rest being shipped to the remaining countries. The reason why we cannot make a great deal out of this quarterly number is that, alike everything here, shipping destination’s composition varies quite dramatically on a quarterly basis. For example, China represented 24% of the shipments in Q2 and Taiwan 34%; in Q1, Taiwan accounted for 49%, while China 8%.

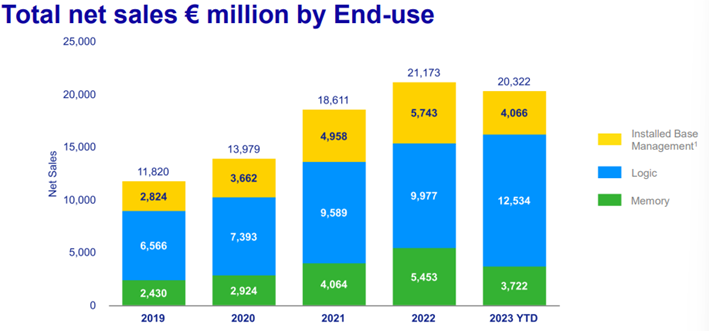

Furthermore, ASML’s sales can also be categorized by the nature of the products’ demand. Logic chips are in charge of processing information while memory chips of storing data. In the last quarter, machines intended to produce logic chips made up for 76% of the total.

Bookings

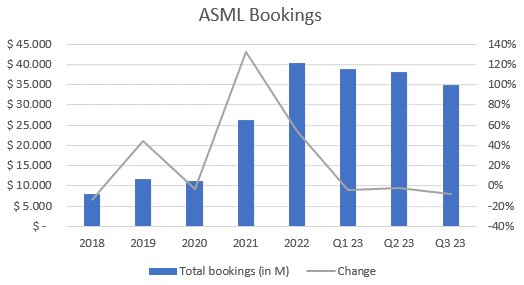

Total bookings is a very insightful variable since it allow us to infer what companies are foreseeing and, from ASML’s perspective, it offers a window into its future topline. Moreover, it sort of shows how resilient could the subsequent quarters for the company be, which, in a downturn cycle for the semi-industry, can prove useful.

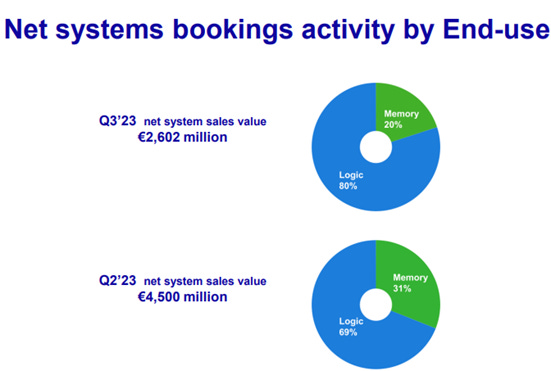

Quarterly net bookings were 2.6bn, of which 0.5bn are for EUVs, finishing a short two quarters of sequential acceleration (Q1 net bookings were 3.75bn and Q2 4.5bn). This is the highest drop ASML’s backlog had had during 2023, giving signs of a persistently uncertain short-term outlook from semi companies.

However, it is worth exposing the superb growth ASML’s booking experienced during 2020-22, having risen by almost 300%. Again, spikes like these, in many cases, simply pulls demand forward, for which short-term new demand can experience some weakness. In any case, backlog is still strong, and it has really helped ASML endure this tough environment.

Finally, ASML’s management team shares the end-use activity by which their systems were booked. 80% of the total 2.6bn are destined towards logic-chip manufacturing, while the remaining 20% for memory.

Capital Return to Shareholders

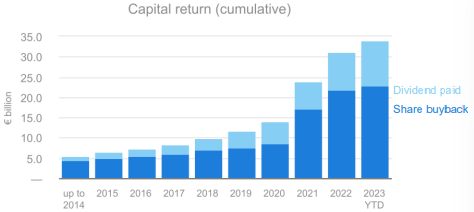

During the third quarter of 2023, ASML repurchased 100M worth of shares and paid 570M in dividends. I must say that, personally, management seems to be deploying capital adequately as to what their repurchasing program respects.

Outlook and Management Commentary

Roger Dassen, ASML’s CFO, covered multiple fronts. He started by laying out what he sees on the Chinese markets and addressed pertinent concerns. Roger mentions that shipments to China are mostly for mid-critical and mature nodes, and that many of these shipments were really booked in 2022 and even prior to that. Something that also contributes to this is Chinese customers’ fill rates. Fill rates have been quite low in the past, but, the recent past shifts in timing of other customers allowed for higher fill rates from Chinese companies. Finally, regarding regulations, his preliminary assessment is that management believes that regulations will not have an impact on overall revenue numbers shared for 2025-2030.

“The main reason being as you know that we make those assessments not on the basis of the bottom-up demand in a country, but really based on the worldwide demand for wafers.”

At the same time, analysts consistently asked what the impact would be, on a more specific basis, on ASML’s business in China. Management responded that something that does not have to escape our attention is that these regulations are mostly about the manufacturing of advanced chips with specific objectives. And a large degree of ASML’s business in China is on mid-critical to mature nodes, which makes the regulations only affect a handful of fabs:

“I think you have to understand where these tools are being used for. The vast majority of our shipments to China is mid-critical to mature. And that’s really where our business is.. there’s a handful of fabs that have been identified as ready for advanced semiconductor manufacturing. So those will – those are now excluded but the vast majority is mid-critical to mature. Will that level off? I don’t think so”.

Dassen then commented on how the current environment looks. The macro is still uncertain and challenging, which is further aggravated by the semi-industry down cycle, they are seeing customers being cautious. Some companies seem to be going over inventories, while others seem to have bottomed out; mixed bag, with overall normalization. With respect to the usage of lithography machines, Roger points out a continued positive development in logic chips, unlike memory. After careful consideration, nonetheless, he thinks that customers “expect an inflection point at the end of this year”, and, despite everything, demand is strong:

“What we do see them do though, is really prepare for continued ramps. So we do see quite a few fabs that are in the progress of being built and we do expect quite some fab openings in the 2024 and 2025 timeframe. Obviously that will require quite some tools"

Turning to their guidance, management expects revenue of 6.7-7.1 billion for the fourth quarter. That would put a 2023’s growth of 30% over 2022, which “I think is a pretty decent performance for the company”. In terms of their longer-term outlook, management remains very confident in ASML’s growth trajectory.

With respect to bookings, Peter mentioned some weakness was expected, more so given how the backlog has built up in the past couple of years. However, given his view on how strong of a year would 2025 be, bookings should recover and start giving those signs throughout 2024, perhaps by the first half already.

My Take

ASML is up to finish a spectacular 2023. The number of factors negatively impacting businesses, and especially semi-companies, are innumerable. Taking into consideration all of this, the fact that ASML has grown at 30%, its backlog remains strong, it has invested to capture the upcoming recovery cycle, and margins have stayed healthy, is remarkable.

The narrative appears to be “concern around the company’s null growth in 2024”, but in the line of the businesses we look for here, this is largely irrelevant. Not only could it have been expected given these past years’ strength, but at the same time, management called for a very strong 2025 and reiterated their 2025-2030 guidance, provided on their investor day in November. The destination remains unchanged, which is what ultimately matters.

For companies, ASML in this case, to remain in their long-term growth trajectory, what’s crucial to determine is whether underlying demand is there or not. In this regard, the secular drivers that are backing up semiconductors’ demand are things that seem inevitable, such as the transition to renewable energy, with EVs leading, electrification, AI, telecommunications, and others. For this reasons, something that stood out was the following:

“Looking further ahead to 2025 we expect a significant growth year since more than 50 percent of our EUV and DUV shipments will go to new fab projects”

Finally, regulations are something that have received a lot of attention lately, for which it was extremely helpful to hear management thoroughly address the issue. The fact that most of ASML’s business in China is not affected by regulations, that this ‘unusual’ exposure as of shipments is not unusual and was somewhat expected due to bookings from 2022 and before, helps in continuing to see ASML’s future. Moreover, I have to reiterate what makes up for 2030’s outlook:

“The main reason being as you know that we make those assessments not on the basis of the bottom-up demand in a country, but really based on the worldwide demand for wafers.”

Personal Commentary

Hope you found the review useful. I’ll be covering many other companies in the next couple of weeks, so make sure to be subscribed to receive them!

Contact: Giulianomana@0to1stockmarket.com

Disclosure: This is not financial advice.

Thank you my friend!