Overall financial analysis

ASML reported results on Wednesday before the market opened. The company generated over 6.74bn in revenue, growing at 91% its topline, which sounds impressive, and it is, but perspective is needed.

(Keep in mind all numbers are in Euros.)

ASML’s financials are quite volatile on a quarterly basis, causing extreme disparities on occasions. In 2021, the company had an average revenue per quarter of 4.4bn approximately, but, in the first quarter of 2022, ASML’s revenue dropped to 3.5bn. That quarter was a very weak one and it’s the one to which the current is compared, making it an easy comp. Nonetheless, the reason why revenue generated is still impressive relies on the fact that ASML continued pushing its quarterly topline to record numbers while the semiconductor industry is going through a down cycle.

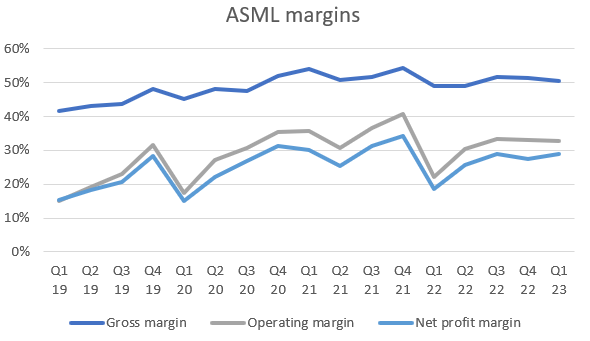

Moving down the income statement, ASML did 3.4bn in gross profit, which represented an increase of 97% YoY. Consequently, gross profit margin expanded 160bps, from 49% to 50.6%. Additionally, the company reported 2.2bn in operating profit, implying an increase of over 280% on a yearly basis and 4% sequentially. This is again due to the extremely weak comp Q1 of 2022 represents, in which ASML’s margin dropped to a multi-year low of 22%. Lastly, ASML generated 1.95bn in net income, implying a net profit margin of 29%.

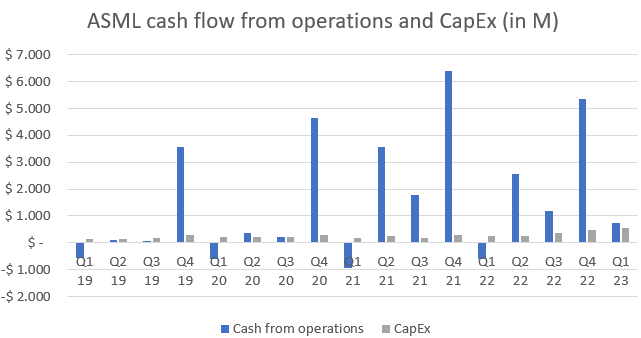

At an operating level, ASML brought in 744M in cash from operations while also having 550M in capital expenditures. That leaves the company’s free cash flow at 194M for the quarter. The chart below should tell how capital light in nature their business model is (at least in CapEx terms), but also how volatile their operating profit is.

Management comments on the subject;

“We continue to expect significant generation of cash in the years to come and the policy hasn’t changed. The policy, just as a reminder, whatever cash is being generated first off we will apply that to the business needs. So whatever capex that we would need, that will be funded from the free cashflow that is being generated by the business. And then whatever remains will be available to the shareholders”

Revenue breakdown

Asml derives revenue from two major sources. The first and main one consists on the selling of photolithography machines while the second one on support, upgrading and selling enhancements to further improve performance of old systems.

In the last reported quarter, 80% of the revenue the company generated came from lithography system sales, while the remaining 20% from their installed base management operations. The trend there as to how much of the total revenue is derived from each segment is also quite volatile, oscillating from 65-35 to 80-20, generally.

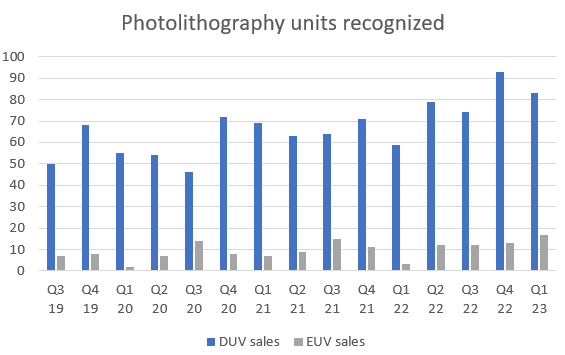

System sales revenue also splits into two main products, extreme ultraviolet and deep ultraviolet machines.

Again, volatility makes system sales be all over the place. As of the last quarter, ASML sold 83 DUV systems and 17 EUVs. This is the quarter in which the company recognized the selling of the highest number of EUV machines (I think) while DUVs were 10 systems off the previous quarter. At the same time, 9 EUV systems were shipped.

The regions to which the company shipped its systems did not change much quarter on quarter. Taiwan is still the country that demands the most photolithography units, representing almost 50% of the company’s total.

Furthermore, ASML’s sales can also be categorized by the nature of the product’s demand. Logic chips are in charge of processing information while memory chips of storing data. In the last quarter, machines intended to produce logic chips made up for 70% of the total units sold.

Bookings

This is probably one of the points that can always be highlighted from ASML’s quarterly reports. Bookings is a very insightful variable since it allows to infer what are companies foreseeing and, from ASML’s perspective, it offers a window into its future topline. Moreover, it sort of shows how resilient could the subsequent quarters be for the company, which, in a downturn cycle for the semi industry, can prove useful.

The company ended fiscal year 2022 with 40.4bn in backlog revenue, number which fell sequentially to 38.9bn. Not many semiconductor companies presented results at the moment so it is difficult to tell how tough is the industry’s environment. However, TSMC reported on Thursday. TSM grew its topline by 3% and all margins contracted across the board. Management said they continue to expect struggle:

“Moving into second quarter 2023, we expect our business to continue to be impacted by customers' further inventory adjustment,"

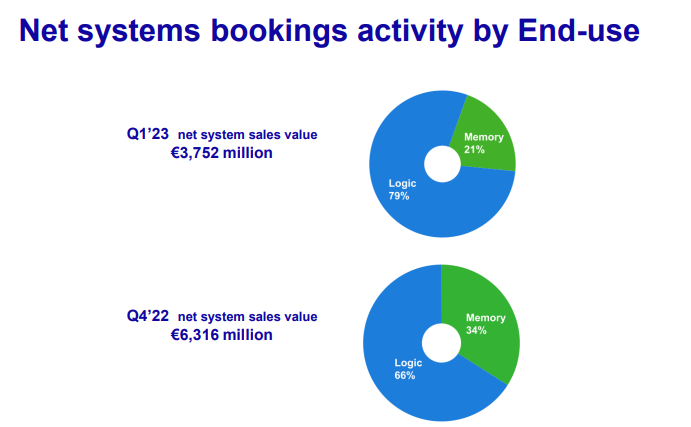

Announcements like that one provides further perspective on how ASML’s bookings act as a sort of cushion. Quarterly net bookings were 3.75bn, down sequentially from 6.3bn, also giving signs of a decelerating demand. Companies ordered a much higher percentage of machines meant for logic chips than before, perhaps anticipating demand of computing power. This could well be due to the rise of AI in 2023, technology that requires very high levels of processing.

Out of the 3.7bn of net bookings, 1.6bn were bookings of EUV systems. I’ll further comment on bookings in the last section.

Capital return to shareholders

In the first quarter of 2023, ASML repurchased over 400M worth of shares and announced their intention to declare a total dividend of 5.8 per share in 2022, implying a 5.5% incresase in resepect to 2021. ASML has now surpassed the 20bn mark in cumulative share buyback and around 8bn worth of dividends paid.

Outlook and management commentary

ASML’s management team expects next quarter’s revenue to be between 6.5 and 7bn, a gross margin of 50-51%, R&D costs of around 990M and SG&A costs of around 275M. For the whole year, they still expect 25% of topline growth with a slight improvement in gross margin. For the fiscal year 2023, they expect to ship around 60 EUV systems, implying a 40% growth, and 375 DUV systems for around 30% growth.

Management mentioned how results were above their own guidance and below it in respect to costs. The only factor that came in below expectations was installed base management revenue due to ‘less upgrades’.

Customers have been experiencing weak demand in consumer driven end markets while markets like automotive and industrials remain relatively strong. In a more specific manner, memory customers are more aggressively lowering CapEx and limiting output to reduce inventory. On the other hand, logic customers are also moderating output for some markets and, in others, demand is still strong so no need of moderation.

“As a result of this market dynamic, we do see customers making adjustments to demand timing relative to last quarter. However, we also see other customers more than willing to absorb this demand change, particularly in DUV”

Demand for lithography systems has been strong for quite some time now, but it has been moderating for the past couple of quarters. During 2022:

“DUV demand was 50 percent higher than our build capacity while this gradually reduced from 30 percent at the end of Q4 2022 to 20 percent at the end of Q1 2023”

A moderation in orders was expected after many quarters of strong bookings, more so considering the environment. Management makes special emphasis on this point considering the long period in which ASML’s backlog cover shipments.

My take

ASML reported a spectacular quarter, very much in line with the last ones. Even though the slowdown in bookings was abrupt, it was mainly due to the environment and, until we get out of it, the company still has its short-term future ‘covered’ with 38bn in backlog. This should help ASML transition out of this down turn cycle in a much smoother way than other semi companies.

Furthermore, all metrics are coming above management’s own expectations and guidance for the year, which was already strong, has been reiterated. Not only this, but this rapid growth is accompanied by margin expansion, which gets to show not only high demand, but an efficient handling of it as well.

As of lithography machines, management talked about how, even if demand is slowing down due to multiple factors, the fact that they have companies ‘more than willing to absorb this demand change’ reveals how crucial of a technology this is and how necessary it is for other companies future plans.

Personal commentary

I really enjoyed putting this article together and will try to expand research and coverage on ASML in the near future. I have many topics I’d like to write about. In other news, I’ll be covering many more companies like Tesla, Microsoft, Visa, Google. If you’d like to receive their ERs review at your email, subscribe below!

Disclosure: This is NOT financial advice.