The test of time is the most arduous of them all. Accumulated judgments lead to finding untruth in elements, and hence their lack of value. In consequence of this consideration, my sense has always guided me towards classics. Every field has them. The likelihood of one learning relevant information in classics is high. Interestingly enough, I recurrently find valuable items in this realm.

Supported by a strong intuition, I’m taking the obverse route today. Even though novelty in most intellectual verticals is, apriori, useless, value can arise occasionally. Antonio Linares is the writer of Investment Ideas. I have followed Antonio’s work for 1.5 years, and after careful meditation, I suspect his investment philosophy is worth examining. He reminds me of Nick Sleep.

Nicholas detected a qualitative business element that had produced immense benefit to its practitioners and shareholders. Namely, scale economies shared. The objectiveness of its core allowed Nick to leverage it in multiple industries. He developed an intellectual thesis that was transferrable due to its industry agnosticism. This insight caused a large breakthrough in my understanding of investing and the mechanisms one can employ for achieving extraordinary returns.

Antonio, in the same line of analysis, is able to submerge in the profoundness of businesses and extract the qualitative variables that have yielded results in the past. Given the unavoidable fact that investing is about the future, Antonio built his strategy by learning how to detect these patterns among new companies. I will go over two of these, as per my understanding.

AMD: Disrupting Nvidia

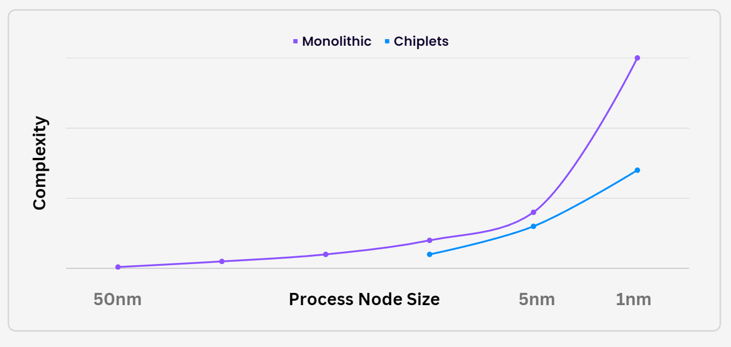

Moore’s law predicts that “the number of transistors per device will double every two years”. The thesis for semiconductors has revolved around compressing more and more computing power in less physical space. In consequence, the size of chips has dramatically decreased, while their capacity increased. Advancements are now facing a wall imposed by physics.

Antonio noticed that the industry is immersed in an unsustainable path. A monolithic approach to chip design and manufacturing has been the norm for the past decades. This entails encompassing increasing amounts of computing power into one chip, made out of a big piece of silicon. Two problems arise from the approach: (i) if one gets something wrong, the whole thing needs to be thrown away; (ii) as chips get increasingly smaller, complexity of design and manufacturing skyrockets.

Therefore, he suspects that “Nvidia’s monolithic approach has an expiry date.” AMD chose another route ten years ago, producing chiplets. I understand chiplets follow a process wherein one breaks down the big chip into smaller components. The objective is to design and manufacture these separately to then put them together.

The chiplets approach seems to solve both problems. If something goes wrong with one of its components, it can be thrown away without losing the rest of the work. Moreover, the granularity compresses the overall complexity of the process. Both elements allow chiplet-based manufacturing to offer the same computing power at a highly reduced cost. They provide AMD with a structural competitive advantage.

The logic behind the thesis for chiplet-based manufacturing begs the question: why hasn’t Nvidia pivoted? And here’s the genius of Antonio.

“the chiplet architecture is not all that easy to apply to GPUs, since they bring about higher levels of latency. When you break down a processor into chiplets, the information takes longer to move around and so the scenario is not black and white.”

“We are not adverse to chiplets, but we are really good at making big dies, and I would say that I think we were actually better with Hopper than we were with Ampere at making a big die. One big die is still the best place to be if you can do it, and I think we know how to do that better than anybody else. So we built Hopper that way” - Jonah Alben, Senior VP of GPU Engineering at Nvidia, seemingly exhibiting a rather typical attitude of a company subject to the Innovator´s Dilemma in this interview.”

Antonio seems to have mastered Clayton Christensen’s theory. His understanding of the semiconductor industry gave him pertinent context to detect whether or not something was happening at the disruption level. My sense is that this is one of the most brilliant articulations I’ve ever read. It requires unbelievable levels of thinking to uncover something like this. Time will tell what happens moving forward, but I genuinely congratulate the man.

Note: His first investment in AMD is up something like 50x and Antonio has written maybe in excess of 100 pages on this. My writing lacks infinite details.

Spotify

Antonio’s thesis for Spotify differs from that of AMD in that it’s not based on The Innovator’s Dilemma. Notwithstanding this remark, they resemble each other due to them possessing the same nexus. Both embody the successful repetition of patterns that have previously worked, which is what I’m starting to label as intellectual theses.

I read Jeff Bezos shareholder letters in February and found an element that kept arising to the surface. Amazon is severely obsessed with its customers. Although I frequently heard about this trait, it was difficult to get the full grasp of it until I read the letters.

Jeff, from the beginning, recurrently went out of his way to deliver a better service for customers. Thinking backwards from customers’ perspectives led him to make multiple decisions that hurt Amazon in the short term. For instance, the company started refunding customers when it didn’t need to.

“Webuild automated systems that look for occasions when we’ve provided a customer experience that isn’t up to our standards, and those systems then proactively refund customers”

“Most customers are too busy themselves to monitor the price of an item after they pre-order it, and our policy could be to require the customer to contact us and ask for the refund. Doing it proactively is more expensive for us, but it also surprises, delights, and earns trust”

In parallel to both factors, the core of Amazon’s business was built around scale economies shared. Every time management performed an efficiency innovation, they lowered prices. Combined, these characteristics and attitude have delighted customers since day 1, turning them into loyal users of Amazon services. Antonio noticed a very similar thing is occurring with Spotify.

“Spotify, like Amazon in its early days, is a misunderstood goodwill compounding machine with the potential to revolutionize the audio industry”

The main constituent of Spotify’s bear argument lies upon the company’s incapacity of producing any profit. In fact, after rapidly rising in 2015-2017, their gross margin has stayed relatively flat at 25%. What Antonio realized is that this has been done on purpose. Spotify’s focus on the customer led them to expand into new audio verticals, audiobooks, podcasts, and education. The service provided to creators has also been a unit of focus. Lastly, as far as my understanding goes, prices have rarely been raised,

“The essence of our business model is to deliver unparalleled value to our user base through an ever improving consumer and creator experience”

In a world where network effects turn competitive landscapes into massive domination, delivering incremental value to customers compounds at unimaginable rates. Spotify has become the leader in its category. Due to the lack of price raising, offering the best ad-terms to creators, and their expansion into margin accretive verticals, Antonio suspects that an invisible free cash flow snowball is rolling.

Final Commentaries

In the foregoing paragraphs, I have stated my understanding of what Antonio Linares’ theses consist of. The common denominator is one that, after reading Nick Sleep and careful meditation, made itself evident to me. These investment theses are not constructed upon normal ground. They are not to be found in financial statements nor in widely spread resources.

I have several reasons to believe that Antonio is operating in another dimension within the investing field, the one in which Nick specialized. My sense is that such waters are the most difficult to navigate. Working by analogy only makes sense once one points them out. It is, however, a fountain from which people can extract unpriced observations, therefore creating a process capable of generating extraordinary returns on a systematic basis.

Personal Commentary

This was an article I’ve had in mind for the past couple of months. I knew it would be a tough one to put together, but I think you’ll understand why I deviated from my usual lines. This is rare and admirable to my eyes. Hope you found the read interesting!

Contact: giulianomana@0to1stockmarket.com

Giuliano, I'm flattered. Thank you for this article!

Hopefully the theses live up to the expectations. Keep up the great work :)

As a fan of both Nick Sleep and Antonio's writings, I must thank you for writing this. The deeper narrative underneath AMD and SPOT are compelling and it shows a next level of thinking. I haven't found the confidence yet to act on it though...