At the end of the day, we want companies that can continuously grow, earn more money over time and make more profit as well. To reach such growth state and perdure in it, a business not only has to perform at a high operating level, but many variables must be correctly handled too. A key factor influencing a company’s future is how skilled and disciplined management is, when allocating capital.

Being in charge of a business is, in an over simplistic definition, leading a group of people and making money-related decisions. Making sure a management team takes good decisions on those regards and manages both fields accordingly, should only increase the percentage of chances we, as shareholders, have of appreciating our money.

Capital Allocation Skills

To evaluate how skilled management or a single person is at allocating capital, one has to try to ‘measure’ how much money are they able to make with the money they have at disposition. In more general terms, it’s about assessing their ability to utilize resources. The more efficiency with which they operate, the more will they generate with less of an investment. This drives a ton of value for shareholders and heavily compounds over time.

The difference between a person that can make 20 cents of profit out of a dollar of invested capital with another that makes 18 cents may not seem much at first. When time goes by, discrepancy between the two grows larger and larger.

Ways to measure efficiency

Return on Equity (ROE) is the net income a company makes in a particular fiscal year divided by the shareholders’ equity invested in the company. It tells you how much money is a company able to make upon the money shareholders invested in it.

Return on Assets (ROA) is the net income a company made in a fiscal year divided by its total assets. This metric reveals how efficiently does the business employ its assets, it tells you how many dollars it makes per dollar worth of assets it has.

Return on Invested Capital (ROIC) is equal to the net operating income after taxes (NOPAT) divided by the invested capital in the business (equity + debt). To clarify a bit more, NOPAT is Operating Income * (1-t).

This metric tells you how many dollars did the company make in a certain period upon each dollar invested in the firm via equity or debt.

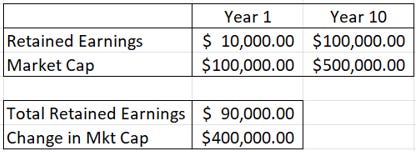

An avenue one can take to check management’s capability of creating value for shareholders is by looking at retained earnings and the value created (mkt cap) during a certain period of time. This allows to infer if the overall market sees value in the actions a company has taken over this defined period, many of which were realized via the earnings management retained. Beware of selecting a short timeframe, in which multiples and prices may go in discordance with underlying fundamental changes.

Source: Self-made

Ways to measure discipline

In general terms, management’s discipline when allocating capital can be evaluated by looking at how do they spend money. A truly disciplined team would only spend money with a clear purpose and with tangible results.

Sales and Marketing are the operating expenses a company ‘chooses’ to have’for it to increase the reach and sales conversion of the different products or even the brand itself. With its purpose clear, you can kind of ‘measure’ the utility of this operating expense by looking at the revenue growth it generated or by changes in the length of sales cycles.

Research and Development is another operating expense a company ‘chooses’ to have. Its purpose is to improve existing products, invent new ones, improve a product manufacturing.

Once identified the different purposes, you know what to look for when assessing this sort of discipline and efficiency. Did the company create new products? Did the company’s margins improve? Did the company improve its business model? This is an example from the research I made on Microsoft:

Source: Microsoft Research, Last Part Taking into account stock-based compensation can let you see what’s the implicit cost shareholders are paying for the growth of the company. It allows you to contemplate things like free cash flow per share, which is a ‘truer’ indication of how much operating money is the business doing and if it is growing or not.

Capital Expenditure can help you identify how asset-light or heavy is the company you are evaluating. Remember this can be defined either as an asset investment or as a recurring expense to maintain facilities. How much CapEx does management need to fulfill both points compared to competition can provide you with a glance of how naturally costly is the business management has built. At the same time, it can be helpful to try determine if such CapEx is being employed wisely, to strengthen a competitive advantage for example, like Texas Instruments, or not.

Personal Commentary

This is an article I’ve had in mind since the beginning of the Newsletter. I find this subject extremely interesting and useful when analyzing businesses. I hope you enjoyed it and, if you have, I post content like this on a weekly basis!

Nice. Explained in a very simple way. Thanks for sharing